Vanessa Quigley Co-Founder Chatbooks Interview

You asked for more content around business finances, so we’re delivering. Welcome to Money Matters where we give you an inside look at the pocketbooks of CEOs and entrepreneurs. In this series, you’ll learn what successful women in business spend on office spaces and employee salaries, how they knew it was time to hire someone to manage their finances, and their best advice for talking about money.

Photo: Courtney McOmber

Vanessa Quigley co-founder of Chatbooks

In an interview with Forbes, you revealed that an intense episode of mom guilt drove you to start Chatbooks. Can you take us back to that moment? What inspired you to launch your business and pursue this path?

I have seven children, and for the first seven years of motherhood, I was very good at scrapbooking our family's story. But things changed as more babies came and as digital photography became the norm. Years later, I found my youngest, who was five at the time, in bed bawling his eyes out. He had been looking at a little photo album his preschool teacher made for him and was moved to tears when he told me, "Mama, I never want to grow up!" It was adorable and a gut punch all at the same time. I wanted him to be able to hold onto more of his memories and knew that I needed to create an easier way to do that for us and families everywhere!

You’re a mom of seven and the co-founder of Chatbooks along with your husband. How has being a mother changed your priorities and your focus in terms of your career? Do you think motherhood has made you a better business person?

My career has actually made me a better mother. I'm happiest when I'm stretching myself, learning, and growing, and I've never felt more stretched before in my life than I have been while building our business. I was a stay-at-home mom for years before becoming an entrepreneur, and motherhood prepared me not only to have my product insight but also taught me the importance of team culture. We refer to our family as "Team Quigley" and I work very hard at helping my children know what it means to be a Quigley and what is expected of them and how important it is that we are all aligned on our goals to work together. And it's the same for our Chatbooks team.

Since launching Chatbooks in 2014, you’ve raised over $20 million in funding from investors. No doubt you’ve learned a lot along the way—What are three crucial elements everyone should include in a pitch deck when raising money and why?

1. How big is this opportunity? How do we know it’s a big opportunity? How can we show that we’re off to a good start capturing that big opportunity? What is our plan to continue and accelerate the momentum we have?

2. Why now? Why is right now the best time to chase this opportunity? Why was five years ago too early? What market change or technological breakthrough makes today the right time?

3. Why you? Why are we going to win versus the next team? What is the founder-market fit story? What secret have we discovered and do we believe in more than anyone else?

What advice can you share for entrepreneurs on partnering with the right investors? What do investors need to bring to the table other than just money?

It is a partnership. At least, that is how we view it. Investors need to bring expertise in some aspect of company building that complements your own team’s current abilities. Also, make sure you are on the same page as far as a timeline. Some investors are in it for the long haul, and some are looking for more of a quick return. Make sure you’re both trying to win the same game before you bring on a new partner.

Where do you think is the most important area for a business owner to focus their financial energy and why?

It depends on your business, but for us, product and marketing have been the biggest areas of investment. When we raised our Series A it was on the strength of our performance and we just needed more fuel to put on the fire. We had a product that worked, and it was great to be able to get more financing to spend on marketing. Your business is going to grow and you will need money to hire a team to support it and to, most importantly, hire the right people—and that is expensive.

What was your first big expense as a business owner and how should small business owners prepare for that now?

Our first large expense was on the creation of our viral “Real Mom” video. To make the video we spent more than we ever had on anything. However, we got back the investment in three days. Today, the video has more than 100 million views.

What are your top three largest expenses every month?

1. Advertising 2. Printing/shipping 3. Personnel costs

Do you pay yourself, and if so, how did you know what to pay yourself?

In the early days, we did not pay ourselves; it was actually a couple of years of no paychecks. And then we went to the bare minimum, enough to sustain life and pay the bills. As the business has grown and we’ve become more profitable, we have gotten a small raise here and there. The real value now is in our ownership of the company.

Photo: Courtney McOmber

Would you recommend other small business owners pay themselves?

If you don’t have to, then no, bootstrap as much as you can. If you can hire and build the business without paying yourself, then don’t pay yourself. The more ownership you can retain the better. For us, we went a couple of years without paying ourselves and by the time we landed on a product that was working, we had to raise money because we had a business team, seven kids, and a mortgage.

Did you hire an accountant? Who helped you with the financial decisions and setup? Are there any tools or programs you recommend for bookkeeping?

In the beginning, we hired an accountant, and then years later, we got someone in-house at Chatbooks. My husband was an accounting major and has an MBA, so finance stuff was the easy part. Making something people want and figuring out how to sell it is the hard part. Do that and everything else will work out. We recommend starting with Quickbooks and Excel, and then when it gets complicated hire an accountant.

How did you know you were ready to hire and what advice can you share on preparing for this stage of your business?

We were trying to build software and we didn’t know how to code so we needed help with the front-end and the back-end. Luckily, we found our first backend developer on Craigslist and he was really, really good and he is still with us today. That is why we couldn’t pay ourselves because we had to hire for the skills we lacked. Be honest with yourself about your skillset and the help you are going to need. Consider possibly taking on a partner. We took on a partner who was a tech wizard and that is what we needed more than anything.

Do you think women should talk about money and business more?

Yes, yes, yes. Women tend to shy away from talking about money. No topic should be off the table. Whenever I interview an entrepreneur on my podcast, “The MomForce Podcast,” I ask them about funding and money matters. I think we should all be more comfortable talking about that.

Do you have a financial mentor, and do you think all business owners need one?

Yes, everyone needs one unless you have a background in that. That could be an adviser, investor, or partner. There are some things that you can do early on in your business that will have real, lasting repercussions. I also suggest hiring a lawyer to help protect your business from the get-go.

What money mistakes have you made and learned from along the way?

We gave some equity to advisors early on. That, in some cases, was really helpful because we could give equity instead of payment, but we had varied success with that. Some people did a ton to help us and were really engaged with us and some, not so much. If I could do it again I would be more careful choosing advisors and working more closely with them. I wish we had set regular meetings with them and gotten more out of the relationships.

What is your best piece of financial advice for new entrepreneurs?

Don’t run out of money. No, but seriously, figure out what is most important in growing your business, and don’t get ahead of yourself. We didn’t have a glamorous office space in the beginning, just a corner with a bunch of desks in a shared space. Today, we have a beautiful office with sweeping views of Utah Lake. When you are going to hire, get the best people. The best is not always the most expensive. If you realize it is not a good fit, don’t be afraid to cut them and start again. A lot of mistakes are made in hiring. Don’t be afraid to say this isn’t working and try again.

Anything else to add?

“The Lean Startup” is the bible. And creating an MVP, a minimally viable product, to test your concept before going all-in is a must. Start small, do a test, see if there is interest. Like doing a pre-sale or Kickstarter, just get really creative to test the concept before you spend. When we started showing Chatbooks to people and they said, “Shut up and take my money!,” we knew we were onto something good and ready to invest.

MORE ON THE BLOG

How Multiple Income Streams Helped This Small Biz Owner Find Freedom

Everyone daydreams about the things they would do and the places they’d go if they had money and the freedom to not work anymore⎯ but as Taylor deDiego has experienced, there are ways to structure your life to accommodate a job you’re passionate about while putting yourself on track to fulfill your dreams. How'd she do it? She found financial freedom through multiple income streams.

deDiego is an accomplished editorial copy director and brand strategist in the beauty industry who began her career at Sephora, working as a copywriter and editorial director for five years. After, she moved to Herbivore Botanicals to lead editorial copy direction. Two months ago she left Herbivore and more recently, she decided to go freelance to be able to work with multiple clients and increase her income stream.

Though deDiego has only had her business for two months, she's already noticed internal and external shifts that reassure her she made the right decision. “It doesn't feel like I have this glass feeling over my head, the way that I felt when I was in a 9 to 5 working for one company. I get to strategically figure out what kind of clients work for me, and how much work can I take on. And then that, in turn, is reflected in financial advances and possibilities," deDiego says. She generously shares her tips and insights into what it’s taken to find personal freedom, by increasing her revenue stream while successfully operating a new small business.

1. Know your value

One of deDiego’s biggest strengths is not accepting breadcrumbs. She stands firm in the value her expertise in her niche brings. “I'm not chasing clients who don't agree with my value,” she says. “What I'm charging is offering you value beyond, ‘Okay, great. We have somebody who's doing our copywriting and we don't have to do it.’ It's like impacting their business as a whole. I know the value of what I'm offering and not just as a service, but what the bottom line is for their business. I know the impact of having strong editorial direction and very strong copywriting.”

This mindset has provided growth in more ways than one. “It's based in neuroscience and reprogramming your brain to really come from a high-value place. And that has been super impactful for me,” she shares. “It has overhauled my entire life, whether it comes down to career, or personal and family relationships. That has been foundational in getting me to a place where I know that I can hold out for the clients that are the most aligned for both, pay and projects, and long-term relationships.”

2. Assess your priorities

For deDiego, as for many, the pandemic “shifted” a lot of things. “I got really clear on what is important to me. What are my long-term goals? What are my short-term goals? And refocusing on a career that felt fruitful and exciting was a place that I found I spent a lot of time thinking about.”

When you get clear on what you want, and even what you don’t want, you can start to intentionally create your life in a way that allows those things the opportunity to come to fruition. “I think that more than anything, I look at this as a real lifestyle shift,” she says. “I just think that it opens up a lot of freedom in my life.”

3. Merge multiple income streams

“I see the potential of how far this can go,” she says, of her ability to earn significantly more than she did at her previous 9 to 5 jobs. Multiple income streams allow her to control working from different places, and she’s planning on using that to her advantage. “I've always wanted to live in multiple cities,” she explains. “San Francisco is my home. It's where my family is. I have a beautiful apartment here! But I can also pick up and go work in New York for a week and be on a client's shoot there, effortlessly and easy.”

Another place on her list that can now be a reality? Paris. “That's the city that I've always wanted to live in again,” she shares. And I'm like, ‘Great. You can go on your quarterly vacation there,’ and spend significant amounts of time, doing the things that really light me up.”

While travel is great, her eyes are also on the future and stability that’s now possible to continue along this path. “And then I think on the longer-term goals, like buying a house always felt like, 'oh my God, how would I do that?'” Now, with multiple income streams, she doesn’t have to worry.

Written by: Abby Stern

When COVID Hit, She Had to Close Her Restaurant—Now Her Products Are Flying Off the Shelves at Whole Foods

And she hasn't taken any venture capital.

You asked for more content around business finances, so we’re delivering. Welcome to Money Matters where we give you an inside look at the pocketbooks of CEOs and entrepreneurs. In this series, you’ll learn what successful women in business spend on office spaces and employee salaries, how they knew it was time to hire someone to manage their finances, and their best advice for talking about money.

Photo: Courtesy of Ayeshah Abuelhiga

Ayeshah Abuelhiga was first inspired to open her own restaurant while working at local eateries in Washington, D.C. as an undergraduate at George Washington University. “It’s where I learned the value of a hard-earned dollar, where I learned Spanish, and where I saw people like me who didn’t necessarily have rich parents with white-collar jobs who paid their tuition,” explains Abuelhiga. “I saw the opportunity for restaurants to modernize, and ultimately, I knew that one day I wanted to own a restaurant." And after 14 years of climbing the corporate ladder, she did finally open the doors to her own restaurant, Mason Dixie, an authentic Southern comfort food hotspot, in D.C.

Although she had the make the difficult decision to close her restaurant after six years of serving the D.C. community due to COVID-19, she’s stumbled upon an even more impactful way to modernize the food industry. Like so many small business owners in 2020, she pivoted, identifying an opportunity to bring the wholesome biscuits that people would line up around the block for in D.C. into frozen food aisles across the county. Today, Mason Dixie has evolved into a clean frozen food company that makes biscuits and breakfast sandwiches that are available at over 6,000 stores, including Whole Foods, Target, Safeway, Costco, and more. And Abuelhiga is just getting started.

Below, the founder tells Create & Cultivate how she’s scaled her company sustainably, why she’s opted to raise funds from private investors (rather than through venture capital), and what major mistakes she’s made and learned from along the way.

You started Mason Dixie, in part, because you believe everyone should have access to affordable, wholesome food. Take us back to the beginning—What was the lightbulb moment for Mason Dixie and what inspired you to launch your business and pursue this path?

I grew up poor. I was raised in low-income housing in Baltimore up until I was 11, but my parents did their best to instill the values of home-cooked, wholesome meals. We shopped at farmer’s markets and bought produce that was bruised, but we ate very balanced meals. I notice now looking back that the kids I still remember that I grew up with in Section 8 that ate out of vending machines are still in the system today, and those who had better access to food, are in better places. You truly are what you eat and I have always believed we deserve better.

In that same vein, my immigrant parents owned a soul-food carry-out restaurant and convenience store when I was little and I got my taste for American cuisine from it. It was also a deciding cuisine when my Middle Eastern dad and Korean mother would disagree about whose cuisine would win out for dinner that night. I craved soul food even as I was coming of age in college, but I could never find homestyle, scratch-made comfort food, only fast food equivalents.

Fast forward to college. I was the first member of my family to attend college and since my parents didn’t make a lot of money, I had to work to pay for school, so I worked in restaurants throughout my years at George Washington University. It’s where I learned the value of a hard-earned dollar, where I learned Spanish, and where I saw people like me who didn’t necessarily have rich parents with white-collar jobs who paid their tuition. I saw the opportunity for restaurants to modernize, and ultimately, I knew that one day I wanted to own a restaurant.

So after working for 14 years in male-dominated industries, like tech and auto, and quickly climbing the corporate ladder, I realized I was an upper-level manager who was unfulfilled and had another 20 years to go before I could go after the only female C-level role that I didn’t even want. I was disenchanted and uninspired. So, I decided it was time to start my dream of owning a restaurant. So in 2014, I founded Mason Dixie. I saw a huge opportunity in the lack of comfort food options available in the growing, better-for-you food space, and an even bigger opportunity making biscuits the focal point since there were no real, scratch-made biscuits on the market. I also saw an opportunity to make scratch-made comfort food affordable and accessible to the masses versus just doing better-for-you food in the fine dining realm by looking at the fast-casual scale and ultimately, grocery, as an even better avenue to do just that.

You recently raised $6.3 million in Series A funding from investors—no doubt you’ve learned a lot along the way. What are three crucial elements everyone should include in a pitch deck when raising money and why?

1. Know the problem you are solving and how big the addressable market really is. Frequently I see founders who do not research the market space enough and show a $20M market opportunity. No investor gets excited about the opportunity to take up to 10% of a $20M market. If you make a seed oil and that segment is small, how big is the oil market in general? Sell the sizzle. It’s the opportunity size that gets early-stage investors going. But be realistic. Be able to defend the market size with real data.

2. Know your sales performance and gross margins inside and out; it is ultimately how investors judge your worth. I cannot tell you how many founders I talk to that don’t even know what goes into a gross margin calculation, or where their strongest sales are coming from. This is important stuff you should be able to spat out on command.

3. Know how you are going to use the funds. Don’t just say I need $1M. What is that $1M built from? Half to overhead/salaries, some to equipment, a third to working capital? Show in your projections how you get to that number. You will always be surprised after analyzing cash flow projections how much more you really need than you thought.

You decided to forgo venture capital and instead opted to raise funds from private investors, many of whom are women. What advice can you share for entrepreneurs, particularly WOC, on partnering with the right investors, and what do investors need to bring to the table other than just money?

I say this until my face turns blue and people still look at me like I have three heads but choosing investors is like choosing a husband. They are almost identical on legal paper. They own your assets, you share financial responsibilities with them, and ultimately your relationship will be what allows you to succeed or fail. They are not a bank or a cash lender; they are meant to be business partners.

You have to know the type of personalities you vibe with, what their values are, do you have the same humor even. It’s like dating. You have to ask yourself, “Could I be with these people forever? Are they my people? Do they really believe in me and what I am trying to achieve?” These are some of the top questions I ask of my investors when getting to know them and I highly recommend founders do the same when they go out to raise. This is why for WOC especially, it’s important to find your people. The check is secondary to shared values and work style.

You launched Mason Dixie in 2014, and now the brand is available at over 6,000 stores, including Whole Foods, Target, Safeway, Costco, and more. What has been the biggest challenge in scaling your business and what lessons have you learned along the way? What advice can you share on how to scale a business sustainably?

The hardest part about scaling a fast-paced growth business is predicting growth. There are times when you get it dead wrong and over-project, and there are times you go gangbusters and hit it out of the park. Both scenarios are challenging to plan for.

I think the way we have navigated our business growth best was by learning the hard way at first and then optimizing each year. At first, we sprinted and made some mistakes. We were lucky in that the sprint just qualified us for the next race, but we weren’t ready. We just happened to be the fastest runner in that first race. I would have preferred looking back to have trained and prepared for the second race.

So with each misstep, we corrected, learned, and analyzed our weak points and then went in more cautiously. We chose better retailers, improved our product mix, then accelerated. I would always make sure to be cautious. If I could do it again, I would win strategically big and focus on making those wins bigger before going wider. It helps mobilize the team better, focuses your assets, and then allows you to move stronger into new markets.

There are a lot of small business owners reading this interview who would love to have their products sold at major retailers like you. How can these founders follow in your footsteps? What advice can you share for getting a foot in the door with a big-name retailer?

Fair warning: the market has changed a LOT since we first got started. Anyone who started before a couple of years ago were the pioneers. You did a lot and asked for forgiveness later and people were more willing to grow/make mistakes with you.

Now, the world has changed. There is a lot more competition—a lot more products out there—and retailers are getting smarter. Before you go pitch to a big retailer, you have to really know if you are ready. Do you have the marketing and trade budget to support the account? Can you keep up with the volume? Can you afford slotting fees? Do you have a sales support team to monitor and manage the account?

Remember, these players have dealt with far more billion-dollar companies than they have thousand-dollar companies, so the rules are set for much bigger fish than you.

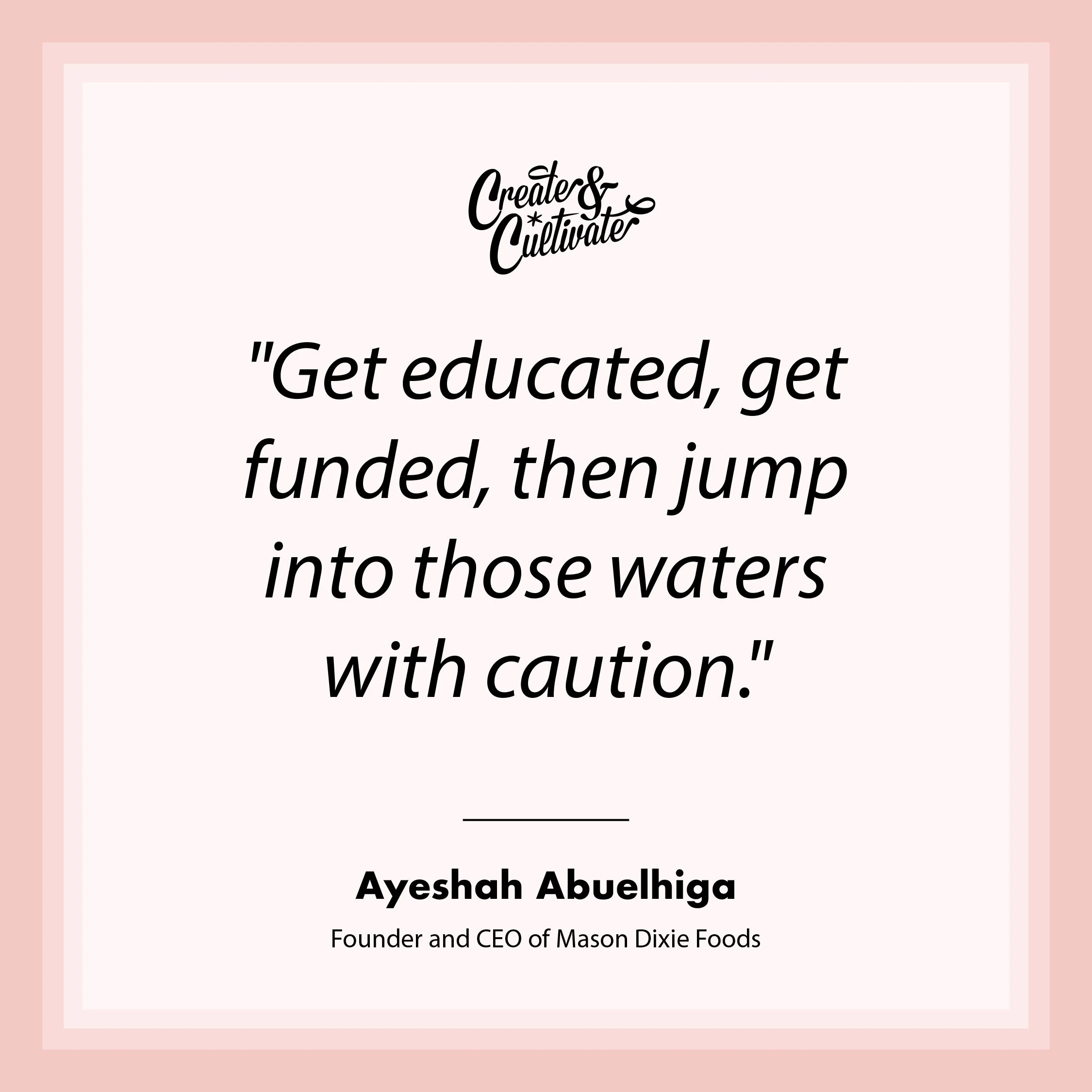

Get educated, get funded, then jump into those waters with caution. Surround yourself with skilled and experienced advisors who have worked in the category/product type you are developing. Ask other companies in those retailers about their experience—both their successes and their follies. Get informed before you pitch.

Where do you think is the most important area for a business owner to focus their financial energy on and why?

Being a founder/CEO means you need to know everything about your business—point-blank. There isn’t one area that is more important than the other. It’s a living system and all parts of the system need to be financially healthy in order for the business to thrive. Now, this doesn’t mean you need to be the expert. Hire a great accountant or CFO early. Allow them to train your eye to see the dark spots and opportunities clearly. Focus on understanding your business over how to be a financial whiz.

What was your first big expense as a business owner and how should small business owners prepare for that now?

People. People people people. They should always be your first biggest expense. Who is helping you to create your projections? Who is going to manage your first order, or even make it? Remember, you cannot do this on your own and the value of the people you surround yourself with will be invaluable in the long run.

What are your top three largest expenses every month?

1. COGs – All of your cost of goods should and will be your largest expense.

2. Trade expenses/marketing – In frozen, we invest a lot into trade since it’s not as easy for us to market and get trial by handing out free sample packs at a metro station or triathlon. Investing back into trade helps us grow and should be one of your largest expenses as you scale.

3. People – Your people should be the best of the best and they deserve to be financially treated as such so they are spending 100% of their time worrying about their business and not if they will get paid. Remember – this industry is tough and financially risky. This is always on the minds of your people so make sure you can pay them on time, and in full.

Photo: Courtesy of Mason Dixie

Do you pay yourself, and if so, how did you know what to pay yourself?

I didn’t pay myself for four years so that others might eat. I lived off of savings and credit cards for as long as I could to ensure I could snag the best people, finance the next purchase order, or invest in the next piece of equipment or manufacturer. I only started to pay myself once I knew I

couldn’t cut checks big enough anymore to fuel the business and took in our first investment, but even then I was conservative and only took what I need to pay rent and eat. As an owner, don’t forget you own the company and that is way more valuable than a salary.

At first, conserve as much cash as you can otherwise you will burn through equity instead. Taking a big salary is a cash burn that will cost you more equity when you need to raise more money before the company has earned the valuation it deserves. So be frugal about what you need in the beginning until the business can afford to pay you.

Would you recommend other small business owners pay themselves?

It just depends on that owner’s personal situation. If I started a business as a single mom with three kids and little savings to live off of, I probably would pay myself the bare minimum I needed to feed my family. But as a single woman with nothing to lose, I lived as bare as I could on what I had. In fact, I worked side hustles until the business could afford to pay for me. It really depends on your financial needs and situation—just be frugal is the biggest advice I can give.

How did you know you were ready to hire and what advice can you share on preparing for this stage of your business?

You are always ready to hire. No one is good at everything. I would have a hard look at your skills and experience, rate those against the different business functions your business needs, and then hire for anything you didn’t rate yourself strongly for. When I took in a business partner, my COO, Ross, I knew I was terrible at operations and needed help. Similarly, when I saw sales ramping up, even though I knew I was good at sales, I only had so much time so rather than spread myself too thin, I invested in the hires knowing that yes, I could still do it, but what was the opportunity cost?

Did you hire an accountant? Who helped you with the financial decisions and setup?

Yes. This should be one of your first hires. I rarely have ever met a founder who is an accountant/financially trained. These people are, you need them. Again, they will educate you about how to look at your business and ultimately help you finance it. They are a critical function.

What apps or software are you using for finances? What’s worked and what hasn’t?

Every business can start with Quickbooks or any off-the-shelf software. In fact, there is a huge market opportunity for you software engineers out there to design scalable accounting software for product companies—hint hint! It’s been fine because of its ease of use and cloud-based

access, but terrible for really using it as a business intelligence and decision support tool. At the end of the day, it’s accounting software, so decision support is still happening in Excel for us. I don’t think there are better solutions until you advance a bit more, but I am always looking.

Do you think women should talk about money and business more? Why?

Yes, we are the biggest consumers in the world! We are business!! More decisions need to be made by the women who LITERALLY hold the purse strings. It can only happen with us talking out loud about it and informing the powers that be how we view money, business, services, etc. The more we show up, the louder we are, the more we will be seen, the more will change.

What money mistakes have you made and learned from along the way?

The funniest mistake was when I thought I was going to be Willy Wonka and open a biscuit factory in just a few months! It was actually one of the best mistakes I ever made. When we sold into Whole Foods our growth was so fast that we were getting requests for products everywhere. Naively, my business partner Ross Perkins and I decided to go after more accounts, particularly in the South because if these biscuits couldn’t sell down there, then we should just call this a good swag item and not further invest. Well, we got both Publix and Kroger to buy our biscuits and were going to go from 100 stores to 1,000 stores in just under nine months. With no idea how to do this, Ross and I leased a drive-thru restaurant with a huge parking lot in the middle of nowhere so we could make pallets of biscuits and store them in a portable trailer freezer on the lot.

We kept doing this for months and transporting the pallets, but the demand kept growing locally, so we couldn’t even keep the inventory we had reserved for the new accounts. I thought we needed to build a bakery! A frozen dough bakery! In the middle of DC! I spent a ton of money on fully engineered plans for this biscuit factory that was also going to have our restaurant attached for the full Ghirardelli experience until we were about to pull the trigger on this huge spiral freezer. Turns out the freezer requires either ammonia or freon—which in DC—are banned in the quantities we needed to fuel this machine. So, we were dead in the water, and we had to pivot to find a way to make biscuits within four months.

I say it was the best mistake I ever made because I ended up being fluent in frozen biscuit production—I knew exactly the equipment I needed, the process, the cost of things—so when I went on the hunt for the facility that would ultimately make our biscuits, I knew everything I needed to know to make the search easy. Because I failed at building a factory, I succeeded in finding the best co-manufacturer out there for our biscuits, and that is what ultimately allowed us to scale and has brought us to where we are today.

What is your best piece of financial advice for new entrepreneurs?

Learn about venture capital and investing before you start. It’s way more complicated, personal, and nuanced than anyone tells you. I did my best to read and research but only as I was hearing no’s during our initial raises. I even did a killer pitch where every investor in the room asked for follow-up discussions. But sometimes it’s not just about your business track record. Sometimes it’s about the color of the money on the table or how much more money is needed and it’s hard to stomach when you think everything else is A+ and you still can’t close the deal.

Anything else to add?

Whenever the going gets tough, ask yourself, what have you ever failed at that you tried your absolute hardest at?

I can’t think of a single time when I put my all into something where I didn’t succeed, so I know if I keep trying, anything can happen. I realized if I didn’t stop trying and if I continued to persevere and stop putting a period at the end of the task, I would ultimately succeed. It’s been the driving statement that through every bad turning point in the path to getting Mason Dixie where it is today, and it is 100% effective.

MORE ON THE BLOG

How to Become a Millionaire and Live Your Dream Life, According to Rachel Rodgers

“Stop making broke-ass decisions.”

What is your relationship with money? Do you live in scarcity mode or do you have an abundance mindset? Either way, we need to get better at talking about money if we ever want to be better at managing it, and eventually having more of it. Well, our new series, The Money Files is set to change all that by helping women become masters of their own finances so they can manage their money and their future.

Imagine having to work eight extra months just to earn the same pay as your white male co-workers. This is the likely reality for Black women in the United States as we marked Black Women’s Equal Pay Day on August 3rd this year. According to the National Women’s Law Center, on average, Black women are paid $0.63 for every $1 their white male counterparts earn. That equates to $964,400 (nearly $1 million) in lost income over a 40-year career.

In honor and support of Black Women’s Equal Pay Day, we spoke with Rachel Rodgers—who's leading the conversation around social injustice and Black wealth—about her mission to change these statistics and close the pay gap. Through her company, Hello Seven, and her recently published book, “We Should All Be Millionaires,” she is empowering other women to hit seven figures by changing their relationship with money, stop procrastinating, and start making million-dollar decisions.

How do you become a millionaire? What does it take to hit seven figures?

These are questions most of us have asked ourselves at least once in our lifetime and while you might think it’s a pipedream, Rodgers is here to tell you that it isn’t. The author, intellectual property lawyer, business coach, CEO of Hello Seven is on a mission to help other women hit seven figures without sacrificing their family or sanity. Over the past eight years, Rodgers has worked with New York Times-bestselling authors, tech startups, coaches, consultants, doctors, accountants, nutritionists, and so many more to take their business to the next level by creating and protecting their own intellectual property to scale their businesses to a million-dollar (or more) enterprise. (She outlines her four steps to becoming wealthy in any climate over on our Ask an Expert series on IGTV.)

In addition to her work at Hello Seven, Rodgers is also leading the conversation around social injustice and Black wealth with her Anti-Racist Small Business pledge. Instead of calling them out, Rodgers is calling companies in to have an honest discussion about racial justice and to help them determine how they can and should be part of the solution—that pledge has been signed by 2,200 businesses and counting.

So, do you want to learn more about Rodgers’ strategy for how to become a millionaire without sacrificing your family or your sanity? It’s time to stop procrastinating and start making million-dollar decisions by investing in yourself to build your dream life.

“One of my s’ heroes, Madam C.J. Walker, became America’s first female millionaire back in 1906,” Rodgers explains. “She was born to slaves. She was poor. She was Black. She was oppressed. She had every obstacle you can imagine and more. All the odds were stacked against her. Yet, she became fabulously wealthy. She launched a haircare company, built her fortune, and provided dignified jobs for hundreds of people. She bettered herself and the world. If she could do it then, you can absolutely do it now. And you can start today.”

Of course, there is no magical solution to gaining wealth but there are fundamental objectives that can help you get there. In the words of Rodgers, “Instead of obsessing about how to trim your budget down to the bare bones, focus on exponentially expanding your income.” And you can start with as little as $100 (or less). Are you ready? Let’s go!

Photo: Courtesy of Hello Seven.

Stop procrastinating

The sooner you start building wealth, the better.

If you’re struggling to motivate yourself to make and save more money, the main thing to remember is that having more money is never really about “the money.” It’s about the people you love and the causes you care about.

Here’s an example: A few years ago, I was traveling out of town for work, and I received a phone call about an emergency situation happening at home. I was immediately panic-stricken. All I could think was, “I need to get home now. Get me on the next flight home. I don’t care what it costs.”

I booked a super-last minute flight with three layovers and it cost $1,700. An outrageously expensive flight, but I didn’t care, and it didn’t matter. I could afford it. No problem. Done.

A typical American does not have an extra $1,700 laying around for emergencies or pleasure or any other reason. And this is a problem.

You need more money because money provides more options for you. The option to fly home immediately if you need to. The option to send your kids to the best school. The option to leave a bad relationship without worrying if you can afford to live by yourself. The option to donate to causes like Black Lives Matter. The option to live as you choose, in freedom, in peace.

Again, if you’re struggling to motivate yourself, remember, it’s not about the money. It’s about the people you love. It’s about the lifestyle you want. It’s about having options instead of limitations.

Look: do you want options, or not? If you do, then get after that coin!

Start Investing

Like so many things in life—jogging, cycling, twerking—investing may seem intimidating at first, but you just gotta dive in and start!

Start small and keep it simple. I love the app called Mint which is a great way to get started with investing. You can start with $100 (or less) and go from there. Once your $100 investment brings you an extra $20 that you didn’t have before, you’ll be like, “Omg, I just made $20 bucks! Yay, free money! I love this!” and you’ll be inspired to keep going!

Make Million-Dollar Decisions

If you want to start earning more money than ever before and build serious wealth, these are the three fundamentals:

1. Stop making broke-ass decisions.

A broke-ass decision (a.k.a., B.A.D.) is any decision that steals your money or steals your time, energy, peace, joy, or power, and therefore, blocks you from becoming wealthy. For example, allowing your spouse (or child) to interrupt you 15 times an hour when you’re trying to work from home, thereby making it impossible for you to concentrate. That is a broke-ass decision. Stop doing that.

2. Start making million-dollar decisions.

A million-dollar decision is any decision that brings you more money, and/or more time, energy, peace, joy, and power. It’s a decision that makes you feel rich—financially, emotionally, or both! Investing in a new blazer that makes you feel like a CEO instead of a shlub? Yes! That’s a million-dollar decision. Raising your hourly rate? Yes. Starting a side-hustle so you can start earning an extra $5,000 per month? Yes. Fueling yourself with high-quality food? Yes. Exercising daily? Yes. The path to millionaire status is paved with million-dollar decisions.

3. Surround yourself with people who are doing it.

Fact: You are heavily influenced by your social circle. For instance, one study found that when low-performing students start hanging out with straight-A students, the low-performing students start scoring higher grades too. Success is infectious. It’s true with grades and it’s true with money, too.

If you want to become wealthy, start hanging out with ambitious people who are already wealthy, or, who are committed to the same goal.

That’s why I launched my Club, a place for women who want to make serious money. Because when you hang out with millionaires and millionaires-in-the-making, the golden-money dust rubs off on you!

Invest in Yourself

To me, “investing in yourself” means doing anything that makes you feel powerful. Because the more powerful and confident you feel, the more money you’re gonna make.

There are infinite ways to invest in yourself, and it looks different for every person.

You can throw out your stained yoga pants and invest in a new wardrobe that makes you feel like a boss. You can invest in hiring a part-time personal assistant five hours a week so they can clear 1,000 tedious tasks off your plate and free up your mental bandwidth. You can invest in education, training, coaching, therapy, or all of the above. What’s going to help you feel your best? Whatever it is, do that.

Swap Budgeting for Expanding

Many people, especially women, are told, “You should go on a diet,” and, “You should cut back on your spending.”

Both of these statements are deeply offensive to me because what you’re really saying is, “You should shrink and make yourself smaller.” “You shouldn’t reach for too much.” “You should find a way to be satisfied with much less.” “You shouldn’t take up too much space.” “You shouldn’t want too much, have too much, be too much.”

Boo to that oppressive patriarchal nonsense!

I take the opposite stance. I say, “How big do you want to live? What’s your dream life?” and then, “Cool, so what’s your plan to make that happen?”

Try this: get a piece of paper and write down everything you would love to have. Your ultimate dream life.

Do you want a three-bedroom house in the best neighborhood in town? Do you want a full-time nanny? A tutor for your kids? A new car with all the latest safety features? Make a list of what you truly want.

Then, take your dream-life-list, head to Google, and find out how much each item costs. Crunch the numbers. Find out what it would cost to have your ultimate dream life. It might not be as much as you think. You might realize, “Huh, okay, my dream life costs $10,000 per month,” or $20,000, or $30,000, or whatever it is.

Once you have this information, it’s empowering, and it leads to new questions. Now you can ask yourself, “Well, what’s it going to take to earn $10,000/$20,000/whatever amount per month so I can have my dream life? How can I pull this off?” Get creative and write down 25 different ways you could earn more and make it happen.

I do this exercise with my clients and it’s fascinating to see what they come up with.

Instead of obsessing over how to trim your budget down to the bare bones, focus on exponentially expanding your income.

Ditch the Debt Stress and Focus on Earning More

Stop stressing about debt, and instead, just focus on earning more money. It’s really that simple.

Start a side hustle. Ask for a raise at work. Double your hourly rate. Text your cousin and tell him it’s time to pay back that loan. Focus your attention, time, and energy on one question: “How can I bring more money in the door?” Focus on that. Get that cheddar. And before too long, you’ll be able to pay off whatever debt you owe.

Learn to Trust Yourself

Taking a risk really just means, “doing something that’s going to change your life in a positive way before you feel totally 100% ready to do it.” And guess what? You are never gonna feel 100% ready. If you’re waiting for that moment of perfect readiness to arrive, it never will. So you might as well take the leap now.

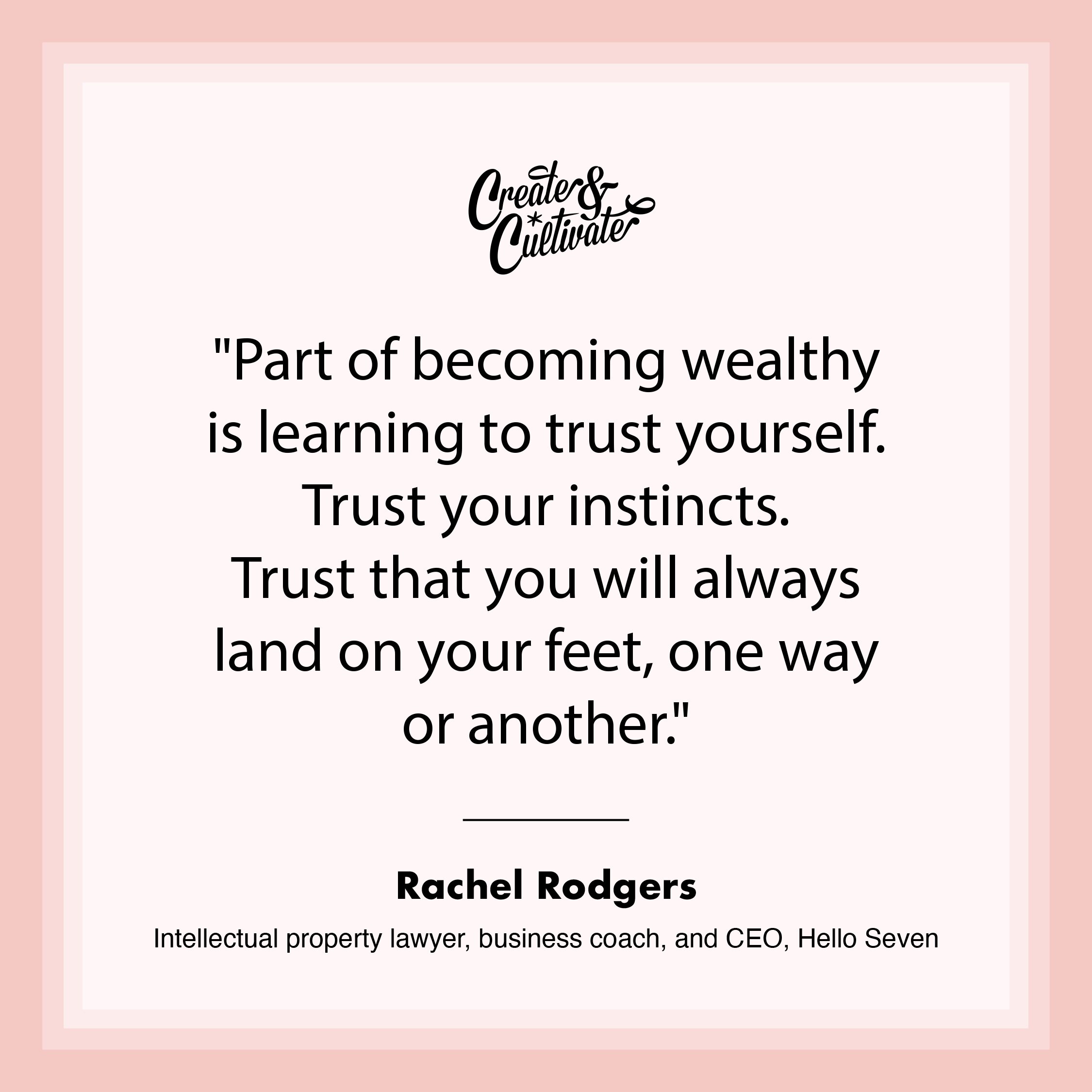

Part of becoming wealthy is learning to trust yourself. Trust your instincts. Trust that you will always land on your feet, one way or another. Trust in your creativity and resourcefulness. Trust in your ability to get things done. By taking a tiny risk now, and thriving, you build a little more trust in yourself. You gain evidence that it’s okay to take risks. This emboldens you to take bigger risks later on. So, start with a tiny risk today and build from there.

Diversify, Diversify, Diversify

I’m all about multiple revenue streams! In terms of how to do this, step one is, you need to leverage your intellectual property. Leverage your what, now? This just means, take something you’ve created (a system, method, process, formula, system, secret recipe, etc.) and package it so that people can purchase it 24/7 even when you’re asleep.

A great example is, let’s say you’re a dog trainer. You have a unique training process that your clients love. They get amazing results and always rave about you but you can only see 10 clients per week so that’s limiting your income.

So, you decide to create an online program (with tutorial videos) so that people all around the world can learn your special process. You sell your program on your website. Cha-ching! You just turned your intellectual property (a.k.a. your unique process) into a cash-generating product.

You might be thinking, “But I don’t have any intellectual property!” but that’s not true. You do. Almost everyone does. You probably have some blind spots and you’re not seeing yourself clearly. Chat with a friend, hire a business coach, or join my Club and you’ll quickly see, “Oh, wow. I’ve been sitting on a million-dollar idea, and I didn’t even realize it.”

Make Wealth Your Reality

What’s a one-million-dollar decision you could make today? One decision (big or small) that would bring more money, or, more time, energy, peace, and power into your life?

Do it. Make that decision. Then another. And another. This is how you will build wealth, and enjoy the freedom and options you want. “Other people have done this, and I can do it too” needs to become your new daily mantra. It’s the truth. And the more fiercely you believe it, the sooner it will become your reality.

This story was originally published on August 13, 2020, and has since been updated.

MORE ON THE BLOG

These Founders Are Bringing Fair Labor Practices, Artisanal Jobs, and Economic Development to Tunisia

Alia Mahmoud and Lamia Hatira are investing in their “tiny but mighty Mediterranean country.”

You asked for more content around business finances, so we’re delivering. Welcome to Money Matters where we give you an inside look at the pocketbooks of CEOs and entrepreneurs. In this series, you’ll learn what successful women in business spend on office spaces and employee salaries, how they knew it was time to hire someone to manage their finances, and their best advice for talking about money.

Photo: Courtesy of Fouta Harissa

When Alia Mahmoud and Lamia Hatira met, they felt an immediate kinship. “We each have a Tunisian father and an American mother and our lives were sort of mirror images,” says Mahmoud. “Lamia was born and raised in Tunis and spent time in Seattle growing up, while I grew up in New York City and spent summers in Mahdia, Tunisia,” she elaborates. Although both women live abroad today—Mahmoud in Miami and Hatira in São Paulo—their families still live in Tunisia, and the textile brand Mahmoud and Hatira founded, Fouta Harissa, is their way of investing in their “tiny but mighty Mediterranean country,” Mahmoud tells Create & Cultivate. But they’re not just investing capital, they’re investing in fair labor practices for the country’s artisanal community.

By working with Tunisian artisans to craft high-quality, hand-loomed textiles, the brand is dedicated to preserving artisanal weaving in Tunisia while also contributing to the country’s economic development. “Unfortunately, Tunisian artisans are generally undervalued and underpaid as the custodians of our cultural heritage,” explains Mahmoud. “We want to change that by bringing the world a modern take on handmade artisanal products that also support fair labor practices, use sustainably sourced materials, and contribute to economic development in Tunisia,” she notes. Not only that but each of the artisans they work with is employed in a full-time position at the brand’s partner workshop and paid an above-market rate that exceeds the living wage.

Ahead, Create & Cultivate asks the co-founders all about how they self-funded the socially-driven brand, why they recommend hiring an accountant ASAP, and what money mistake has taught them the biggest lesson.

How did you fund Fouta Harissa? What were the challenges and what would you change? Would you recommend your route to other entrepreneurs?

Lamia Hatira: We started with a small friends-and-family investment of $20,000 which helped us start our entities in both Brazil and the U.S.A. We are definitely still working on a small budget. It’s challenging because you don’t have the resources to do everything you want to do right off the bat, but it’s also kind of wonderful because you learn what really matters for your business and how to make the most of what you have.

Each experience is definitely unique, but if you have an opportunity to get seed investment from friends and family at the initial stages, embrace it. Just make sure you’re on the same page with your investors about how active a role they will play and get in writing in your operating agreement.

The most important thing is to do what you’re comfortable with. We knew we weren’t ready to take out a huge loan or ask for a larger amount at the beginning because we didn’t want to owe anyone money or give away too much equity before we knew more about the intricacies of our business.

Three years later, we are now ready to take on more investment because of everything we’ve learned and because we know what works and doesn't work for Fouta Harissa at this stage.

What was your first big expense as business owners and how should small business owners prepare for that now?

Alia: Legal fees to register our business and write an operating agreement, as well as placing our first major product orders with our manufacturer were definitely our first big expenses. I would advise taking the time to build a business plan in order to price out these early costs to the best of your ability, from there figure out where that money is coming from. A great way to generate some early cash flow is to do a friends-and-family sale before your product launches officially. This can help you raise some money and generate buzz.

Lamia: Beyond your most basic costs, make sure to include the other expenses that will ensure that your first customers get the experience you want them to have when they receive their product. This not only includes the product itself and its shipping, but the packaging, the marketing, the communications—they add up.

What are your top three biggest business expenses every month?

Alia: Beyond paying for production, our biggest monthly expenses include the shipping costs to send our Foutas to customers, digital ads on Facebook and Instagram, and investing in regular digital marketing and PR.

Do you pay yourselves, and if so, how did you know what to pay yourselves?

Lamia: Not yet! We’re working on it.

Would you recommend other small business owners pay themselves?

Alia: Absolutely. When it’s your business, you’ll work harder than you’ve ever worked on anything else before. Your time is valuable. Your effort is valuable. Build it in from the beginning. One thing we didn’t take into consideration, that we wish we had, is the employee taxes a business incurs in order to draw a salary. Even as founders! So until you’re making enough profit to distribute in those early years, build a small salary into your costs plus taxes.

How did you know you were ready to hire and what advice can you share on preparing for this stage of your business?

Lamia: You don’t have to go from being a founding team to hiring a staff of full-time employees. We work with a lot of brilliant people, mostly as independent contractors. At this early stage in our business, it gives us the flexibility we need to try new things, learn, and try again. We’re so grateful to the talented people who believe in Fouta Harissa enough to devote their time to growing this business with us.

I think you know when you’re ready when you realize you don’t know how to do everything, and that’s okay! We’re still in the process of learning exactly what our strengths are as co-founders and when and where it makes the most sense to invest in a new skill versus finding an expert who can help. We look forward to the day when we can have full-time staff on the team.

Did you hire an accountant, and if so, would you recommend hiring an accountant to other small business owners?

Alia: 100%. We recommend hiring an accountant as one of the first things you do. They can even advise you when you’re registering your business. We asked around and got recommendations from other female business owners until we found ours.

What are some of the tools or programs you use to stay on top of your business finances?

Alia: Quickbooks has been a lifesaver. It’s a worthwhile investment and makes your accountant’s life a lot easier come tax time. We also use Square for offline payments and inventory tracking. And of course, Excel—a classic—where all the planning and projections happen.

Where do you think is the most important area for a business owner to focus their financial energy on and why?

Lamia: I’d say focus your energy on product quality and your people. Your product has to be the best possible thing you can put out into the world. At the end of the day, if you don’t have a great product, you don’t have a business. Just as importantly, invest in relationships. They are everything, especially at the beginning. You might not always be able to pay everyone you want to but be creative. Find ways to uplift them, involve them in decisions, consult them, and barter with them.

Do you think women should talk about money and business more?

Alia: Definitely. We’re always worried about speaking up because we think everyone else has it all figured out. When you’re a small startup, you think there’s no way others have made the same mistakes that you have. But if we can talk about it more openly, with no shame or pretense, then we can really support each other to make the best and most savvy money decisions.

The reality is, without good finances, there is no good business, and some of us can really use all the help we can get.

Do you have a financial mentor, and do you think business owners should have one?

Lamia: We have two. One on the more day-to-day financial management who helps us build spreadsheets, come up with pricing strategies, and analyze reports; and another one who advises more on visionary planning and fundraising. Both are women and both are total badasses.

Business owners definitely need a financial mentor, or more. Find as many quality mentors who care about you as possible, and cultivate those relationships.

What is the biggest money mistake you’ve made and learned from along the way?

Alia: Underestimating the cost of digital marketing. As an e-commerce brand, we definitely did not anticipate the challenge of competing with companies putting in $10,000+ into social media advertising every month. When you’re just starting out with limited budgets for digital ads, it can be hard to compete. This became even more acute during the pandemic because everyone became an e-commerce brand and doubled down on digital. My advice would be, plan for a bigger budget for ads early on or find creative ways to not rely on them like collaborations, partnerships with brick and mortar stores, and investments into your most loyal customer base to encourage repeat buys.

What is your best piece of financial advice for new entrepreneurs?

Alia: Whatever price you’ve determined for your product, double it. Seriously, there are so many costs you don’t even know exist, beyond your COGS, when you launch a new product. All of those should be built into your MSRP. And do as solid a financial plan as you can.

Anything else to add?

Lamia: If finance is your thing, use it to your full advantage and help others out. If financial matters don’t come naturally to you, make sure you learn the basics of your business finances to always know what’s going on, and surround yourself with people who know what they’re doing and who you can learn from.

MORE ON THE BLOG

5 Black Financial Educators Who Are Empowering Us to Take Control of Our Finances

Teaching us how to budget, pay off debt, and more.

Photo: Courtesy of Tonya Rapley

Welcome to 5 for 5, where we spotlight 5 women in 5 minutes or less.

It’s no secret that Black women are not paid fairly. On average, Black women are paid 37% less than white men and 20% less than white women for doing the same work, according to LeanIn.org. But despite the stats, Black women *can* build wealth. Ahead are five financial educators who are advocating for change, empowering women to take control of their finances, and pushing these stats in the right direction.

1. Dasha Kennedy

Dasha Kennedy, a.k.a. @thebrokeblackgirl, doesn’t hold back when it comes to sharing tips for assessing personal debt, reaching a big financial goal, and implementing a financial wellness self-care routine.

2. Tonya Rapley

The “Millennial Money Expert” and founder of My Fab Finance, Tonya Rapley, is on a mission to help 100,000 people make at least one money decision they’re proud of, whether it’s buying a home or saving money on a trip.

3. Tiffany Aliche

Known as @thebudgetnista on Instagram, Tiffany Aliche breaks down big goals like building wealth, paying off a mortgage, and buying a home while paying off student debt into achievable (dare we say simple) steps.

4. Marsha Barnes

The brains behind @thefinancebar, Marsha Barnes is a must-follow for friendly reminders to engage with your finances, adjust your budgeting plan, and start an emergency fund, as well as tips on how to follow through.

5. Jamila Souffrant

The founder of @journeytolaunch, Jamila Souffrant, is all about helping people grow their savings, get out of debt, and gain financial freedom and independence. (Psst… her podcast, Journey to Launch, is a must-listen!)

MORE ON THE BLOG

Attention, Self-Employed Bosses! Here Are 4 Tips for Budgeting on a Variable Income

Money mindset is everything.

Photo: ColorJoy Stock

During my first month as an entrepreneur back in December of 2018, I made $226 as an administrative assistant. Fifteen months later, I would go on to quit my day job and make upwards of $5,000 a month as a freelance writer and content creator for Rosetta Stone.

While I had excitedly waited to get to this point, it was still hard for me to give up the financial security of my day job. Without corporate perks like PTO, health insurance, and automatically deducted taxes, I suddenly had to make sure I had enough to get through the expected—and unexpected—costs each month without the help of a regular paycheck.

As an entrepreneur or freelancer, it is completely normal to have an irregular income, but it can definitely make budgeting your money a little trickier. Luckily, after a lot of trial and error and some helpful advice from a top-notch financial coach, I can finally say I’ve figured out how to budget with a variable income. Since this is something I wish I had known years ago, I decided it was time to share with my fellow business owners!

1. Calculate Your Monthly Needs

Before taking control of my budget, I had no clue how much I really spent per month. Like most young business owners, in my first two years of business, I was pretty much taking whatever job I could get—mostly because I just needed to get my bills paid. Never really knowing how much to expect from month-to-month, I ignored my bank account completely.

Every month I would just cross my fingers and hope I wouldn’t get an “insufficient funds” notice from my bank. But, this method led to a lot of extra stress and negative emotions around money.

So, one day, I sat down and went through my last three months of bank and credit card statements and looked at how much I had been spending on necessities. This helped me figure out how much I really needed to be making each month to get by. Some common needs within a personal budget include things like:

Rent

Utilities

Groceries

Gas (only for required outings)

Debt repayments (minimum required payment)

Phone

Personal care (toiletries, medicine, etc.)

Insurance (car, life, etc.)

Essential family expenses (childcare, clothing, etc.)

I also included the needs I had for my business. Some common business needs within a budget include things like:

Employee/contractual worker wages

Website hosting

Email hosting

Insurance (health, business, etc.)

Public relations

Marketing/advertising

Business-related debt repayment

Travel

Taxes

Business-related software (accounting, email management, website building, social media marketing, SEO, project management, CRM, communication/messaging, etc.)

Business-related hardware (computers, phones, printers, etc.)

And this isn’t just what I learned from personal experience. When I sat down with financial coach Yvonne Tran for one of my podcast episodes, she echoed this sentiment as well. “If you have variable income my biggest tip would be to know how much you need to pay every month for expenses or bills and make that a goal to bring in every month in your business,” Yvonne shared.

2. Reset Your Money Mindset

Like it or not, we all have certain ideas about money. Whether you grew up hearing “money is the root of all evil,” “a penny saved is a penny earned,” or any other common money-related beliefs, our society has a lot of positive and negative associations with money.

Having grown up in a family of entrepreneurs, money struggles—and the negative money mindset that comes with them—were no stranger to me. For a long time, money was something that I considered stressful and even dirty. It wasn’t until I learned to see money as a tool and something to be grateful for that the money really started flowing.

“Money mindset is definitely really important because if you view money as so stressful, super complicated, and intimidating then I can show you all the ways that you can fix your financial situation, but if your mindset is telling you ‘no’ then it’s not going to work out in the end,” Yvonne told me.

A few ways you can reset your money mindset are:

Using positive affirmations around money (and putting them everywhere!)

Learning to give money away without fear

Evaluating your beliefs around money

Actively fighting off any negative thoughts about money

Fostering gratitude in every transaction

3. Cultivate Healthy Money Habits

Creating a strong budget and resetting your mindset creates a strong foundation for making good financial decisions, but keeping up with those good financial decisions means you have to cultivate healthy money habits too. Some healthy money habits that could help keep your budget on track are:

Downloading a money-tracking app like Mint

Spending with gratitude, not fear by using affirmations like, “I am grateful for all that money brings me,” or “I am grateful that I can contribute my money to the economy/this cause/this person,” when spending money

Setting financial goals each quarter

Waiting 24 hours before buying “wants” to avoid impulse purchases

Saving 20% of your income for the unexpected

Yvonne is a big proponent of saving, especially when you have a variable income. “If you happen to have a short month one month and not bring in as much as you need then hopefully you’ll have that extra savings already set aside,” she shared. “That way, that can come in to fill the gap for that month, and then you’ll just work harder next month to bring in more money.”

4. Re-Evaluate Your Budget Each Month

If you have a variable income it is best to evaluate your budget pretty frequently. By re-evaluating your budget more often, you’ll have a better handle on your money as your income changes.

Since I can usually predict my income for the next few months, I tend to re-evaluate my budget each quarter, but monthly works great too. Here’s the method I use: first, I calculate how much I’ll be making over the next three months. Then, I divide that up to give myself a general monthly budget. Finally, I calculate all of those personal and business needs we talked about earlier.

Next, I subtract my needs from my income and I use that final number as my budget for the month. I’ll usually take out a percentage for savings, but the rest I let myself spend freely. Some people prefer to take their savings directly out of their income, but it makes me feel better knowing everything else is taken care of first. This works well for me because on good months I can splurge on certain items, whereas on not-so-good months I have to reign myself in a little bit. But either way, it gives me a concrete number to focus on each month.

There are hundreds of ways to budget your money, but the best budget is the budget that works best for you. I tried a lot of budgeting methods before I found one that really worked for me, so don’t get discouraged if you struggle a little bit. For me, once I changed my mindset around money everything changed, so I would definitely suggest digging into your own stories around money before getting started. Happy money-making!

“There are hundreds of ways to budget your money, but the best budget is the budget that works best for you.”

—Calli Zarpas, Founder of the Do Well Department

About the Author: Calli Zarpas is the founder of the Do Well Department, a holistic business program created to help overwhelmed business owners cultivate a business and life they love. When Calli isn’t running her community, she’s writing her weekly newsletter and hosting her podcast called Unstrictly Business, all about how successful business owners foster success in both their business and personal lives (Yvonne’s episode is an awesome place to start!).

Love this story? Pin the below graphic to your Pinterest board.

MORE ON THE BLOG

How to Triple Your Revenue in 2021

Simple, proven strategies for hitting that bottom line.

Photo: Smith House Photo

Let’s talk about revenue.

Building a business means setting aside time to map out revenue goals and growth strategies. Which can be a daunting task if you’re a dreamer with big financial goals for your business this year.

For those of you looking at your current balance sheet and wondering how in the world you’ll get there by the end of the year, I’m breaking down a few simple, proven strategies you can implement to see massive growth in hitting that bottom (or top) line.

1. Raise your prices.

Want to know the #1 way to increase revenue without adding additional work? RAISE YOUR PRICES.

Spend an afternoon doing a little internal audit of your services, products & pricing. Determine how many clients you need to book or products you need to sell this year to reach your stretch revenue goals. If it’s a lot...as in, that amount of work will leave you completely burnt out, it’s time to start charging more.

For example, if this year’s annual revenue goal for your design agency is $100,000 and your average service costs $2k, you will need to book 50 client projects this year to reach your goal. However, if you start charging $10k for that same package, you only need 10 clients. And if you book 50 clients, you’ll make $500,000 in revenue. Simple. But hugely profitable.

If you’re wondering if it’s time to raise your prices, here are a few things to consider…

What is the value of your product or service?

The first thing to look at when deciding to raise your prices is the value your service or product holds for your customers. Will your offerings allow them to raise their prices? Sell more of their products? Book more clients? Reach new audiences? Gain new opportunities? Automate their processes? The list goes on.

For example, we have seen our clients double their revenue and quadruple their client roster after working with us. We've seen them go from being a brand nobody has heard of to an iconic leader in their field. The websites we build for our clients have the potential to bring in hundreds of thousands of dollars in sales. We've helped our clients organize and effectively present information that's saved them time and money answering emails or hopping on long sales calls.

Your prices should reflect the value and ROI your product or service brings.

Are you presenting your brand in a way that LOOKS as valuable as it is?

How you present & position your offerings is EVERYTHING. Presentation adds perceived value. There is a reason why beautiful things cost more - they look more valuable.

Your potential clients and customers probably don't know how good your product or service is yet. All they have to go off of is the way it looks.

So ask yourself...

If I knew nothing about my brand, would I pay top dollar for what I'm selling?

Do my offerings look as high value as they are?

Do I stand out and compete with other brands in my industry?

If you answered "no" to any of those questions, it might be time to consider investing in a rebrand. You are probably leaving a lot of money on the table, purely because you don't look like the high-value brand or expert that you are.

What does the experience feel like for your customers?

What happens after the customer buys? Will their experience after purchasing reinforce their decision to buy from you? Was the experience one that will make them want to buy again? Will they tell their friends or colleagues about you?

The customer experience after purchase is just as important. For service-based businesses, this comes through in your client process, the way you communicate, how well the client feels taken care of and how your service is ultimately delivered. For product-based businesses, this is your unboxing experience, the culture you're creating, on-going customer exclusives and how you're building brand loyalty.

Oftentimes, the customers you already have are your best customers. How are you taking care of them and making them feel valued after they’ve purchased?

2. Invest in education.

New skills can help you reach more people, uplevel your current offerings and better establish yourself in your industry. If you want to increase revenue, you should continually be learning and developing your skills.

Start by identifying areas of your business that you wish you knew more about. Or think about services that would complement what you currently offer to offer clients and customers even more support.

Here are a couple of great needle-moving skills to invest in learning…

Marketing & Sales

Facebook Ad Management

Brand Strategy

Copywriting

Basic Graphic Design

3. Outsource and invest in support.

If you see growth in your immediate future, you will need to invest in additional support. As your business scales, so should your team. And as scary as it feels, you need to hire help before the growth comes so you’re ready when it does.

Start making decisions as your next-level self. This will allow you to grow faster, become more efficient, and handle even more growth in the coming year.

4. Develop content & products for a new audience.

Spend 20 minutes this week scrolling through your social media followers. Get to know them. Are your products or services for them? If 20% or more of your followers aren’t your ideal customer, you are leaving money on the table.

Take some time to think about a new product that you could offer. These people are clearly interested in something you currently do. But you haven’t given them an opportunity to convert.

Never underestimate the power of simply listening to what your audience is asking for. It’s probably something completely different than what you think you should offer. Or servicing a new audience entirely. But it will be the most aligned thing you ever do for your business.

Increasing your revenue means trying new things, taking new risks, and learning more than you ever have had before. Step into your next-level self and create a scalable path to revenue growth.

“New skills can help you reach more people, uplevel your current offerings and better establish yourself in your industry.”

—Ariel Garcia, Graphic Designer and Founder of ByAriel

Photo: Clarin J Photo

About the author: Ariel Garcia is a self-taught graphic designer and founder of the creative agency, ByAriel. She is committed to pushing the boundaries of creative innovation and carries that into each project, campaign, or brand she’s a part of. She also mentors graphic designers on developing their own unique style and artistry. Ariel’s typical day consists of several cups of coffee, logo designing, collaborating with clients, styling products, and planning her next adventure.

Love this story? Pin the below graphic to your Pinterest board.

MORE ON THE BLOG

5 of Your Most Pressing Money Questions–Answered

It always pays to plan it forward.

Photo: ColorJoy Stock

COVID has shown us how quickly unexpected events can throw our plans off course. Now, more than ever, it’s important to plan ahead–especially when it comes to your finances. Whether you're bootstrapping your business, setting up your retirement fund, or simply learning the financial basics, it pays to pay yourself forward. Investing in your future will pay back dividends.

To help you master your own financial future, we teamed up with Ally for our recent Money Moves digital summit to host a mentor power-hour with five financial experts to answer your most pressing money questions.

In case you missed it, we’re sharing a few of the Q&As from our Money Moves mentor session. Read on for some sage financial advice from our five mentors who know quite a bit about the importance of investing in yourself, your business, and your financial future.

Jack Howard serves as the Senior Director of Wealth Advisors Operations for Ally Invest. In this role she manages the day-to-day operational processes of the Wealth Advisor business. She is also responsible for the Ally Invest Inclusive Wealth strategy that is part of the Ally enterprise Financial Social Inclusion (FSI) efforts and serves as secretary for the Ally Charitable Foundation. Prior to joining Ally Invest, Jack served as Senior Director of Ally Corporate Citizenship. She was responsible for the creation and execution of strategic programs for the organization’s financial literacy program, corporate giving initiatives and employee giving/volunteerism programs.

Jack graduated from Michigan State University with a Bachelor of Arts degree in Journalism and is currently a student in Syracuse University’s Master of Science in Communications Management program. An active professional, Jacqueline is a member of Alpha Kappa Alpha Sorority, Inc. and Jack and Jill of America, Inc. She also serves on the national board of directors for the American Bankers Association Foundation and Society for Financial Education and Professional Development (SFEPD), as well as the Boys and Girls Club of SE Michigan.

Jacqueline has a deep passion for helping Brown and Black communities build wealth through economic mobility. Her work has earned her a spot as one of the 15 women on the inaugural Next list - an extension of the American Banker Most Powerful Women in Banking program.

Q: Investing can be intimidating–what advice do you have for someone who’s new to investing and doesn’t know where to start. How do I overcome the intimidation factor?

JACQUELINE: As a first-generation stock investor, I know what it feels like to be paralyzed with fear because you don’t know what to do first. I am the daughter of a police officer and teacher who had pensions to fund retirement, so the stock market was not a topic of discussion at my dinner table during childhood. After graduating from college, I realized the importance of owning stocks as a piece of my wealth building strategy. I started small and made a $25 contribution to the 401K provided by my employer. As my salary increased, I contributed more, hired a financial advisor, and opened a Roth IRA account. I also worked hard to eliminate credit card and student loan debt. Over time, I became obsessed with understanding money and wealth building. Now, I am constantly listening to audio books and podcasts, watching CNBC or reading the Wall Street Journal and Barron’s. All of those efforts helped me to better understand money and investing. So, my top tips for new investors: start small, automate the process and make a commitment to learning.