How to Hire the Right People to Take Your Biz to the Next Level With Founder and CEO of Rowan

ABOUT THE EPISODE

Ask any founder: When you’re running a business, hiring is tough. And hiring the right people to take your business to the next level even tougher.

On average, it takes an average of 36 days to hire a new employee. And filling a position doesn’t guarantee success. Nearly half of all new hires fall through within 18 months.

Thankfully, on this episode of WorkParty, Louisa Serene Schneider shares how she successfully hired the right people to grow her business—and how you can do the same.

The founder and CEO of Rowan, a piercing company that’s reshaping the industry, has hired a team of over 45 employees and has over 700 employees working in studios across the U.S.

We about about how she built her impressive business, including her hiring strategy, her tips for retaining employees, and so much more

RESOURCES

To connect with Louisa Schneider click HERE

To connect with Jaclyn Johnson click HERE

To follow along with Create & Cultivate click HERE

To submit your questions call the WorkParty Hotline: 1-(833)-57-PARTY (577-2789)

LISTEN TO THE EPISODE

OTHER EPISODES YOU MIGHT LIKE . . .

Brand DNA: Why It’s Important and How to Define (and Stay True to!) Yours

The Founder of the Astrology App Channing Tatum, SZA, and Issa Rae Love on Launching a Five-Star App

How MaryRuth Ghiyam Went From Owing $700K to Building a $100 Million Wellness Empire

How Fitness Entrepreneur Megan Roup Used Social Media to Turn The Sculpt Society Into a Hit

Karen Perez Launched Second Wind on Instagram—Now Her Products Are Stocked at Saks Fifth Avenue

THIS EPISODE IS BROUGHT TO YOU BY . . .

Babbel • Right now, when you purchase a 3-month Babbel subscription, you’ll get an additional 3 months for FREE. That’s 6 months, for the price of 3! Just go to Babbel.com and use the promo code PARTY.

5 Takeaways from This Founder's Path to Building a Rosé Empire

Rose Gold Rosé is the third evolution of my career. What I have learned over the course of my career is that passion trumps skill (well most skills, anyway). If you do not have passion for the business you are creating, what is going to push you to the next level? What is going to make you feel better when you miss your son’s football game? Your drive will persevere the challenges you will undoubtedly face as an entrepreneur. But it is ok! Everyday is about learning, developing your passion and earning the title of “expert.”

You don't have to be an expert but you have to have the passion to become an expert. What started as a rosé to enjoy with my friends has turned into a lifestyle brand with distribution in fourteen states with over 11,000 cases sold and more coming this winter into the first quarter of next year. Throughout my path, I have been lucky enough to be inspired by so many female founders and the below are key takeaways from my experience and path to becoming a rosé boss.

#1 Passion is a Skill Set

For me, the challenge of an industry I had zero background in — along with no experience in business or ever having been an entrepreneur — was a major mountain in front of me I had to scale. And I did it one step at a time. There was no map, no help, just figuring it all out as I went. There was no other choice — to figure out how to sell this wine or fail. I read everything I could get my hands on about how to start a small business, I have listened to tons of podcasts of female entrepreneurs over the course of the last three years, I have reached out to as many people that I could that were willing to try to give me advice or direction.

At the end of the day, it’s up to you to get it done. The lesson here is — you don’t have to do what your degree (or degrees) hanging on the wall says. You can reinvent yourself as many times as you want. It’s never too late to start over or start anew. I was a family nurse practitioner. Then I was a stay-at-home mom. Now I own my own business. It’s wild but you can do it if you really want to and have the passion to do so.

#2 Surround Yourself with People Who Are Experts

When I started Rose Gold, I knew what I wanted to create and knew how I could fill a void in the market space. What I didn’t know is how to buy grapes or how to produce a product with shelf appeal. Within the first few months, I surrounded myself with the industry’s best of the best. Together, we built a plan to create a classic dry Provence rosé with a beautiful pale pink in color with aromas of rich, fresh fruits, followed by hints of white flowers and minerals. When approaching the experts, be honest. I walked in with my hands in the air asking for help. What I have learned is that people are attracted to passion. The group we pulled together saw my passion and my drive to build a lifestyle brand centered around spending time with the ones you love and enjoying experiences. Also, take every networking meeting/coffee/phone call, because you never know what connections you’ll make or what small tidbit of information you could takeaway.

#3 Let The Answer “No” Be Your Driving Force

Don’t be scared of the answer “no,” but rather let it be your driving force. Over the years, I have received valuable feedback and a ton of “no’s.” When I first started, I made a promise to myself to remain authentic in the process of building my brand. With every no, it has further contributed to staying the course. It is easy to get bogged down and discouraged when you are turned away from an opportunity that you thought could work - only use this as motivation to push past it and keep putting yourself out there. Don’t let that one “no” make you think everyone in that office/organization/industry feels the same way. You could easily receive a “no” from one person in the same place, and the next person you talk to says “yes.” Just keep pushing, do not limit yourself, and you’ll find someone to resonate with you.

#4 Time is Your Most Precious Resource

As a mother of three and building a business, I have come to realize that my time and schedule commitments are precious. It takes alot to raise a family and build a brand. A mentor once told me, it is ok if you do not get everything done in a day and strive for significance over success. I realized that if I was careful with my time and boundaries I could be significant in my day and then weeks. In order to be present with my kids in the morning, I now wake up an hour earlier. This is my most productive time.

As a mother of three and starting my business from the ground up, I have come to realize that my time, schedule, and commitments are incredibly valuable. Building a brand and raising a family are not that different, as both require a lot of time, energy, and nurturing in order to be successful. To pass down some wisdom from a mentor, not everything needs to get done in a day and it’s ok to strive for significance over success. This helped me realize that if I’m more mindful with my time and boundaries, I can be more significant in my days, which carries into weeks, and into months.

When it comes to time, sometimes it requires you and your goals to meet each other half-way. My personal example of this is waking up an hour earlier each day, which allows myself to be present with my kids in the morning. Oddly enough, this has now become my most productive time of the day. This just goes to show that every day is a constant reminder of how precious your time is.

#5 How to Become The Expert

Building something worthwhile is a marathon, not a sprint. It won’t happen overnight and no one is going to hand you your big break. Just keep going every day and push forward — even on the days you want to throw in the towel, remember you are one-step closer to your goals. When I started Rose Gold, I talked to everyone and read everything. I was not an expert in wine, but more so an expert in what I knew I wanted to build. Don’t forget it takes time. Your empire will not come overnight, but rather soak in every opportunity to further your growth to expert level. I carry around a notepad in my purse and if anyone sparks an idea, it goes down on paper. I now have a collection of over a dozen notebooks all around my house. Write it down, learn your craft and the expert title will follow.

About the author: Born and raised Texan Casey Barber is a lover of all things food and beverage-related. Falling in love with the South of France on a trip in 2004, Casey founded Rose Gold in 2017, with her first bottles launching to the consumer market in 2018.Casey is a single mother to three children – Sam (13) Charlie (11) and Gigi (9). Outside her love for rosé, Casey’s interests include culinary experiences, travel and tennis.

5 Numbers to Consider When Launching a Coaching Business

Set yourself up for success.

Photo: ColorJoy Stock

The coaching industry is one of the fastest-growing sectors with the market size predicted to surpass $20 billion by 2022. (Calendar check, it’s already August.) And while this has left many frustrated and floundering in an overcrowded market, it has also jump-started thousands of budding entrepreneurs’ coaching careers.

And as with any new career trend, along with all the commotion, there is a lot of information (and misinformation) floating around the internet. While click-bait Facebook ads often depict building a coaching business to look like a walk in the park and endless traveling, the reality can often look a bit different.

Rather than sitting on a beach, spicy margarita in hand, glancing down at your phone while yet another effortless sale hits your bank account, new coaches and coaching side-hustlers are often found drowning amongst a sea of other coaching connoisseurs, endless freebies, masterclasses, and promo threads.

If you are coaching curious, a coaching side-hustler, or looking to launch (or re-launch) a new coaching business, here are five numbers to consider to ensure that you’re setting yourself up for success, and profit, from the get-go (so that dream of sitting on the beach is a much closer reality.)

Number 1: Your Net Income

How much do you want to make per year?

Have you ever taken the time to really think through the income that would sustain and fund your ideal lifestyle? If not, now’s the time!

This number will largely differ based on where in the world you live, and what constitutes a dream lifestyle for you. For some, it encompasses travel. For others, it’s as simple as being able to afford childcare. Either way, the first number to get clear on, is how much money you need in your bank account in order to thrive.

Example: I need $75,000 a year in my personal bank account to live my dream lifestyle.

Quick definition from Investopedia: Net income (NI), also called net earnings, is calculated as sales minus cost of goods sold, selling, general and administrative expenses, operating expenses, depreciation, interest, taxes, and other expenses.

Number 2: Your Total Cost of Doing Business

What will your expenses and taxes look like?

How much does it cost to run your business? If you have no idea what these numbers are, it’s time to PAUSE and do a little research. For business expenses, outline one-off costs, such as building a website build, and reoccurring costs like accounting software.

For taxes, it’s going to largely depend on the type of business you file and what state you live in. However, for example, expect around 30% of your profits to go to the government. So, multiply your desired net income by .30 to get this number.

Once you know your one-off costs, your recurring expenses, and your estimated tax payouts, you can add them together to get to an estimated “total cost of doing business.”

Example:

One-off costs: $4,000

Recurring monthly costs: $2,000 ($24,000 annually)

30% of 75,000 (net income): $22,500 (taxes)

Total cost of business annually: $50,500

Number 3: Gross Annual Sales

How much does your business need to make?

Now that you have your goal net income, and your estimated total cost of doing business annually, we can add them together to determine what your business needs to generate in gross sales annually in order to support your net income.

Example:

Total Cost of Business ($50,500) + Net Income ( $75,000) = $125,500 = Gross Sales

Quick Definition from Investopedia: Gross sales is a metric for the total sales of a company, unadjusted for the costs related to generating those sales. The gross sales formula is calculated by totaling all sale invoices or related revenue transactions. However, gross sales do not include the operating expenses, tax expenses, or other charges—all of these are deducted to calculate net sales.

Number 4: Gross Monthly Sales

How much do you need to gross per month?

If you were to work for a company, there are generally 52 pay periods in a given year. When you own your own company, you can either payroll yourself OR pay yourself out via owner’s draws. For “Number 4,” you can either divide your total annual gross sales by 12 months OR by 52 pay periods.

When you’re starting out, let’s say as an LLC or sole proprietor, it’s more common to look at your expenses and sales monthly, thus we’re going to use 12 for this example. You want to know how much your company needs to gross monthly in order to deliver you your desired net income. So, simply divide your gross annual sales by 12 to learn what you need to gross monthly.

Example:

Gross Annual Sales Needed = $125,500.00 / 12 = $10,458.33

$10,458.33 = Gross Monthly Sales Needed

Number 5 (Option 1): Total Client Load

How many clients do you need to take on to hit your income goal?

There are two different numbers you can choose to act as your key fifth number (a.k.a. Number 5). The first is your total client load. In this scenario, ask yourself, how many clients do you want to work with at any one given moment? Do you want to only work with three clients annually? Or do you want to work with 30 new clients a month via a group program? You might not immediately know, but pick a number to start out.

From here, you will be able to determine how much you need to charge per client per. For example, if you identified you only want to work with three clients annually, then that means those three clients need to produce $10,458.33 of gross monthly sales for you. That means each client needs to be on a $3,486.11 monthly retainer.

On the flip side, if you have identified you want to go after a volume model, and you’ve identified you want to work with 30 clients a month every month, each client will need to pay $348.61 monthly in order to hit your gross monthly sales goal ($10,458.33 / 30 clients a month = $348.61). However, also consider that this means you need to sign a total of 360 clients annually (30 clients monthly x 12 months).

Number 5 (Option 2): Pricing First

How much should you charge for your services?

If you already know that you’re looking to create a very specific product at a pre-identified price point, then you can back your way into knowing exactly how many clients you need in order to hit your gross sales goals. For example, if you want to sell a $100 online course, then take your total needed gross sales and divide that by $100. This will indicate that you need to sell 104.16 (round it up to 105) courses a month to hit your sales goals.

The Bottom Line

Ultimately, these five numbers are what you need to know in order to identify your ideal business model. Numbers 1-4 inform us of what we need in order to “play around with” Number 5. If you’re feeling stuck between high volume or high ticket, consider asking yourself this, which business model and workload is most conducive to your dream lifestyle? If you need a little more help breaking this down, check out our free masterclass here.

We’ll leave you with this, “living your dream life shouldn’t be just a dream.”

About the authors: Lexie Smith (pictured left), named “Brilliant PR Expert” and “Trailblazer Women Leaders in 2021,” is a PR coach, host of the “Pitchin’ and Sippin’ Podcast,” co-founder of Ready Set Coach, and the founder of THEPRBAR inc., an online coaching brand that empowers entrepreneurs to increase their influence, impact, and revenue through relationship-driven marketing and PR.

Emily Merrell (pictured right), as featured in Refinery29, Girlboss, Forbes, and Huffington Post, is the founder and community curator of Six Degrees Society, a professional speaker, host of the “Sixth Degree Podcast” business coach, and co-founder of Ready Set Coach.

MORE ON THE BLOG

How to Professionally “Break Up” With a Client

Cutting ties is tough, but worth it.

Photo: ColorJoy Stock

As a business owner, your natural inclination may be to please clients, and it can be tempting to fall into the trap of taking any client that wants to work with you. The hustle is addictive. And the thought of saying “no” is scary, especially when faced with the uncertainty of when your next client will be locked down. But while cultivating and growing your clientele, your list of frustrations might follow suit.

PSA: There will likely come a time when you’ll want to cut ties with some clients. It might be something you’ve been considering for a while now as a result of clients behaving badly (hello, unpaid invoices), or maybe you’ve simply become too busy and need to edit your client base (high five, boss). Whatever the reason, it’s uncomfortable AF. And considering your reputation is on the line, you’ll need to finesse this difficult convo.

So to help you manage your business relationships and determine which clients are giving you good vibes and which ones deserve “goodbyes,” we spoke with Andrea Crisp, a life coach, host of "The Couragecast," and author of “Designed With Purpose.”

Is it time to break up with a client?

According to Crisp, here are six signs you are subconsciously done with a client:

1. You feel completely drained after having a conversation with them because you rehash the same thing over and over.

2. You work overtime trying to please them when it becomes apparent no one can satisfy them.

3. You find yourself watching the clock every time you have a meeting with them.

4. You believe there is no amount of money in the world that makes working with them worthwhile.

5. You contemplate going back to your 9-to-5, just to escape this client’s requests.

6. You stop billing them in the hopes that they don’t contact you again.

And here are six signs that a client is giving you life:

1. You are willing to put aside time to work on a project; in fact, you look forward to it, even on weekends or at 3 a.m.

2. You feel compelled by the cause and are passionate about the impact it is making.

3. You are fueled by every conversation. Every time you speak with the client you are motivated and energized and feel even more creative.

4. You think of ways to help them, even during your “me” time.

5. You are on the same wavelength and kinda want to be their BFF.

6. You are willing to go the extra mile for them, even though it’s not part of your mandate.

How do you break up with a client (and prevent it from happening in the first place)?

If you’re starting to feel the “cons” outweighing the “pros,” it’s time to release these clients—and release yourself in the process.

Here are some ways to do so:

Set boundaries right from the start

This not only helps you as an entrepreneur, but also gives clear guidelines to your clients as to when they can expect work to be done, and when they can expect you to respond to their emails, texts, and calls. So you avoid receiving emails on weekends (if that’s not part of your mandate) and avoid anxiety-inducing emails with subject lines that read: “Urgent: need this ASAP.”

“At the beginning of every client relationship, I outline a clear coaching expectation so that my clients are aware of how this relationship will work,” explains Crisp. “It has served me in so many ways. And, I have to constantly remind myself that even if I don’t think a client needs to hear my expectations, I need to say them. It keeps me in check and accountable to my clients, and allows them the freedom to ask the right questions.”

Know your niche

Your dream clients are ideal because you’re passionate about helping them, and your expertise matches their needs and vision. As soon as you take on clients outside of your niche, you have to work harder than ever to figure out what they may need. This becomes super frustrating, as there starts to be a disconnect between your “dream clients” and your “dreaded clients.”

Release yourself from the pressure

Crisp puts it clearly: “Release yourself from the pressure that you need to be everything to everyone. As entrepreneurs, we may want to have all the answers, have the biggest client roster, and have a strong social media following, but in the end, that does not produce results and only pushes us closer to burnout and fatigue. The biggest obstacle that stands in our way of making an impact as female entrepreneurs is ourselves.” Boom.

Give yourself a break, allow yourself to have a day off, turn off your phone. The world will not end. Trust.

Look at your numbers

If you know you simply can’t even with this client anymore, look at your upcoming projects and revenue. Can you afford to let this client go? If this customer is draining you of all your energy and not allowing you to perform at your best, then it sounds like letting them go will help open the window for other awesome clients. And, after all, good clients lead to other good clients. If the client is mistreating you, then you’re better off without them.

Have the difficult conversation

Don’t procrastinate; the longer you put off the inevitable, the harder it will become to have “the talk.” After all, there are times in every relationship, like with your squad, team, or clients that you have to tell the hard truth. This may involve being honest and vulnerable, which can be very difficult.

Face it head-on, take a deep breath and stand tall—you’ve got this.

Don’t look back

Once you make your decision and fire your client, don’t look back. See the situation as a key learning for the future. Upwards and onwards. Trust the process.

When is enough, enough?

The moment you start to believe that you need to fill your calendar with clients out of your niche is the moment you have to work double-time to accommodate their needs.

Don’t go there.

When trying to determine “the last straw,” you have already passed the point of no return. This may sound counterintuitive, but the real question you need to be asking is: “Do you have the confidence and assurance you need to only take clients you want?’

TBH, it really is more about you than them. Ask yourself these tough questions and don’t become addicted to the hustle by taking clients that drain your energy and creative flow.

Another key point is that as you grow, your focus might narrow, which can lead to some clients no longer matching your brand. Recognize when this happens, too, no matter how lovely the client might be.

Remember, a client-supplier relationship is a partnership. And if you’re no longer satisfied with your end of the deal, it might be time to say, “K, bye.”

About the author: Karin Eldor is a coffee-addicted copywriter with a long-time love for all things pop culture, fashion, and tech. Ever since she got her first issues of “YM” (remember that one?) and “Seventeen” in the mail, she was hooked on the world of editorial content. She's a contributor to Forbes, Coveteur, MyDomaine, and more.

This story was originally published on November 28, 2016, and has since been updated.

MORE ON THE BLOG

Is Upstate New York the New Silicon Beach? 3 Founders on How Moving From the City to the Country Benefited Their Biz

Entrepreneurs are flocking to this incubator haven.

Upstate New York has always been a haven for creatives, and when COVID hit in 2020, many founders relocated from New York City to upstate out of necessity, desire, or both. Below are profiles of three entrepreneurs—Trinity Mouzon Wofford, the founder of Golde, Eliza Blank, the founder The Sill, and Hillary France, the founder of The Wylde—who made the move from the city to the country last year. Read on to discover how the change impacted these founders and their businesses.

Trinity Mouzon Wofford, Founder of Golde

Saratoga Springs, New York

During the summer of 2020, when COVID was surging, Trinity and her fiancé Issey, the cofounder of Golde, spent the summer in Saratoga Springs to gain some relief and safety from the intense situation in N.Y.C. They were going back and forth from Saratoga to Brooklyn, a three-and-a-half-hour ride each way, when Trinity had the realization that, for the time being, it made sense to return full-time to upstate New York to live and run their business.

On one ride down from Saratoga during late summer, she remembers thinking to herself that she needed to go back; that perhaps running her superfood health and beauty startup, Golde, and paying rent in Brooklyn for too little space was not benefiting the growth of her business nor her own personal growth. On top of these challenges, Trinity and Issey are in an interracial relationship and, in the city, tensions were becoming palpable during the summer of 2020 in response to the BLM movement and the upcoming election. In a way, she felt as though the systems of the city were starting to fail her and she needed to actively change her surroundings for the benefit of herself, her family, and her business.

Trinity grew up in Saratoga Springs. In fact, four generations of Trinity’s family have lived in the same house that she returned to, where her mother still lives. Returning to the house that her ancestors had lived in for generations felt very natural and provided a safe space to gain a fresh perspective. It’s allowed her to go deeper into outlets such as gardening and plant care, which, in her own words, have allowed for more creativity. Not surprisingly Golde has benefited from this positive energy and change.

During this past year, Golde has been lucky. The business hasn’t been negatively affected, and has, in fact, thrived. In January, Golde launched in Target, and one of the brand’s two new products scheduled for release in 2021, Shroom Shield, has launched. The team has always been remote so no adjustments were needed in order to keep the business running smoothly. The lack of pressure to be everywhere and do everything, something that anyone who lives in a big city can relate to, has allowed her to realize that she can’t predict the future. She can only think a few steps ahead, and for the first time, she is living in the moment and is fully enjoying it and the lack of pressure this brings.

Eliza Blank, Founder The Sill

Stone Ridge, New York

It’s a similar story for Eliza. Coincidentally, both she and her husband Steve grew up in more rural areas of Massachusetts, so the desire to feel the grass under their feet has always been there. She found herself at NYU for university, and although she loved the city, she always missed nature. It’s this love of nature that inspired her to start The Sill, an online plant nursery that delivers botanicals right to your doorstep. It also inspired her to buy her first home in Stone Ridge, situated in the Catskills, in 2015.

The paths to starting The Sill—as well as finding a house in upstate New York—were not straightforward ones. Eliza found raising money for The Sill to be challenging. Venture capitalists often want fast growth at all costs, and Eliza was committed to making sure her foundational economics worked, which, for her, meant slower growth with her eye on profitability from day one. After an arduous raise, she is confident they found the right investors for The Sill, and these investors have been by her side navigating the most difficult year yet. As was the case for most businesses, March 2020 was a very dark time. All five of The Sill’s stores were closed and the distribution center in California was forced to shut down. The bright spot is that sales didn’t suffer. As it turns out, people look to plants for emotional support, and since people could not be together, they found connection in giving small gifts of kindness in the form of plants to each other.

In 2015, when buying their house upstate, Eliza realized that their mortgage would be less expensive than their rent in the city. Little did they know that five years later this house would become their permanent residence, sanctuary, and office for over a year. The past 18 months have led her to question if the social convention of the office is necessary. Does the team even need a five-day workweek? Eliza has started to hire permanently remote team members as far away as Hawaii and the business’s headquarters are now fully remote. For Eliza, she firmly believes that the space and closeness to nature their home provided them mitigated the extreme pressure and stress she experienced during COVID as a leader and also as an Asian American woman. Her home upstate became an oasis from what the world had become, or perhaps further revealed, that we live during a time of extreme unrest and racism.

When asked what’s next for her and her business, Eliza responds that she wants to live a life well-lived. She wants her two-and-a-half-year-old daughter to have the space to play and become independent. For the business, she wants to further realize the broad ways in which nature can be infused into our homes and what the brand essence of The Sill is, and how it can evolve to fit into this new space that we have all found ourselves living in. For Eliza’s family, they will go back to the city for a year in the fall and see how it feels. For right now, the country has allowed her to have creative breakthroughs and reimagine how The Sill can further help us maintain our well-being within our home as we spend more time there than ever before.

Hillary France, Founder of The Wylde

Hudson, New York

Hillary had always thought she would make the gradual move from spending weekends in Hudson, New York to living there full time. What she could not have predicted was that this move would happen as abruptly as it did in March 2020. For seven years, through her company Brand Assembly, Hillary had been running trade events for some of the most enviable fashion brands. Her business had been thriving, and then, within the first month of COVID, the Brand Assembly’s trade show business was almost obliterated.

She saw an 80% drop in activity and she soon found herself in the position of having to reimagine her whole business model. She immediately gave up her office, attempted to pivot but was unable to make it work, and slowly drained her resources. She had to accept that perhaps this almost fully offline and in-person event business was not an operation that could survive a pandemic. Not surprisingly, for the last year, her trade show business has been on hiatus (and the good news is that they are set to return in October of 2021), however, the backend operations piece called The Faculty is still fully functioning. This situation could have fully devastated Hillary, but instead, it pushed her to finally pursue a dream she had always had: to create a space for brands and community to convene in one place in Hudson. At that point, she had nothing to lose so she packed her bags, gave up her N.Y.C. apartment, and moved to her weekend house in Hudson to create what is now called The Wylde.

Hillary had spent nine years going back and forth to Hudson and saw an opportunity for a retail annex in this quickly growing city. In fact, Hudson was recently ranked the #1 metro area in terms of the biggest change in net migration. With the influx of people to the area, she figured there was more of an opportunity than ever to create a space where people could feel a sense of community and continue to be inspired by fashion and conversation. On April 17, 2021, Hillary launched the Wylde’s first outdoor market Summer Saturdays with a selection of handpicked vendors across apparel, accessories, vintage, and apothecary. Local N.Y. brands like M.Patmos, Hudson Hemp, and Lail Design are featured within the market while the permanent retail store that opened on April 30th launched brands like Rachel Comey, Dôen, Mondo Mondo, and more.

Is The Wylde solely an upstate dream? In Hillary’s mind, it’s not. When taking the Amtrak train down to the city she has daydreams of opening The Wylde up in another emerging market if she finds success in Hudson. Rather than feeling consumed by the fashion space she feels excited about how fashion, culture and even coffee (a Wylde cafe is slated to open in August 2021) can bring people together to create community and meaning. This evolution of the business more truly reflects the changes she has felt personally this past year and the community that she had always sought to be a more permanent member of.

Melissa Grillo Aruz, Founder of Aruz Ventures

About the author: Melissa Grillo Aruz has been an active part of the New York startup ecosystem for the past 20 years having senior roles at Forerunner Ventures, Gilt Groupe, and more. She currently runs her own marketing and talent consulting business under www.aruzventures.net where she helps commerce companies scale their business. She currently splits her time between upstate New York and Brooklyn. Instagram and Twitter @melgrilloaruz.

MORE ON THE BLOG

When COVID Hit, She Had to Close Her Restaurant—Now Her Products Are Flying Off the Shelves at Whole Foods

And she hasn't taken any venture capital.

You asked for more content around business finances, so we’re delivering. Welcome to Money Matters where we give you an inside look at the pocketbooks of CEOs and entrepreneurs. In this series, you’ll learn what successful women in business spend on office spaces and employee salaries, how they knew it was time to hire someone to manage their finances, and their best advice for talking about money.

Photo: Courtesy of Ayeshah Abuelhiga

Ayeshah Abuelhiga was first inspired to open her own restaurant while working at local eateries in Washington, D.C. as an undergraduate at George Washington University. “It’s where I learned the value of a hard-earned dollar, where I learned Spanish, and where I saw people like me who didn’t necessarily have rich parents with white-collar jobs who paid their tuition,” explains Abuelhiga. “I saw the opportunity for restaurants to modernize, and ultimately, I knew that one day I wanted to own a restaurant." And after 14 years of climbing the corporate ladder, she did finally open the doors to her own restaurant, Mason Dixie, an authentic Southern comfort food hotspot, in D.C.

Although she had the make the difficult decision to close her restaurant after six years of serving the D.C. community due to COVID-19, she’s stumbled upon an even more impactful way to modernize the food industry. Like so many small business owners in 2020, she pivoted, identifying an opportunity to bring the wholesome biscuits that people would line up around the block for in D.C. into frozen food aisles across the county. Today, Mason Dixie has evolved into a clean frozen food company that makes biscuits and breakfast sandwiches that are available at over 6,000 stores, including Whole Foods, Target, Safeway, Costco, and more. And Abuelhiga is just getting started.

Below, the founder tells Create & Cultivate how she’s scaled her company sustainably, why she’s opted to raise funds from private investors (rather than through venture capital), and what major mistakes she’s made and learned from along the way.

You started Mason Dixie, in part, because you believe everyone should have access to affordable, wholesome food. Take us back to the beginning—What was the lightbulb moment for Mason Dixie and what inspired you to launch your business and pursue this path?

I grew up poor. I was raised in low-income housing in Baltimore up until I was 11, but my parents did their best to instill the values of home-cooked, wholesome meals. We shopped at farmer’s markets and bought produce that was bruised, but we ate very balanced meals. I notice now looking back that the kids I still remember that I grew up with in Section 8 that ate out of vending machines are still in the system today, and those who had better access to food, are in better places. You truly are what you eat and I have always believed we deserve better.

In that same vein, my immigrant parents owned a soul-food carry-out restaurant and convenience store when I was little and I got my taste for American cuisine from it. It was also a deciding cuisine when my Middle Eastern dad and Korean mother would disagree about whose cuisine would win out for dinner that night. I craved soul food even as I was coming of age in college, but I could never find homestyle, scratch-made comfort food, only fast food equivalents.

Fast forward to college. I was the first member of my family to attend college and since my parents didn’t make a lot of money, I had to work to pay for school, so I worked in restaurants throughout my years at George Washington University. It’s where I learned the value of a hard-earned dollar, where I learned Spanish, and where I saw people like me who didn’t necessarily have rich parents with white-collar jobs who paid their tuition. I saw the opportunity for restaurants to modernize, and ultimately, I knew that one day I wanted to own a restaurant.

So after working for 14 years in male-dominated industries, like tech and auto, and quickly climbing the corporate ladder, I realized I was an upper-level manager who was unfulfilled and had another 20 years to go before I could go after the only female C-level role that I didn’t even want. I was disenchanted and uninspired. So, I decided it was time to start my dream of owning a restaurant. So in 2014, I founded Mason Dixie. I saw a huge opportunity in the lack of comfort food options available in the growing, better-for-you food space, and an even bigger opportunity making biscuits the focal point since there were no real, scratch-made biscuits on the market. I also saw an opportunity to make scratch-made comfort food affordable and accessible to the masses versus just doing better-for-you food in the fine dining realm by looking at the fast-casual scale and ultimately, grocery, as an even better avenue to do just that.

You recently raised $6.3 million in Series A funding from investors—no doubt you’ve learned a lot along the way. What are three crucial elements everyone should include in a pitch deck when raising money and why?

1. Know the problem you are solving and how big the addressable market really is. Frequently I see founders who do not research the market space enough and show a $20M market opportunity. No investor gets excited about the opportunity to take up to 10% of a $20M market. If you make a seed oil and that segment is small, how big is the oil market in general? Sell the sizzle. It’s the opportunity size that gets early-stage investors going. But be realistic. Be able to defend the market size with real data.

2. Know your sales performance and gross margins inside and out; it is ultimately how investors judge your worth. I cannot tell you how many founders I talk to that don’t even know what goes into a gross margin calculation, or where their strongest sales are coming from. This is important stuff you should be able to spat out on command.

3. Know how you are going to use the funds. Don’t just say I need $1M. What is that $1M built from? Half to overhead/salaries, some to equipment, a third to working capital? Show in your projections how you get to that number. You will always be surprised after analyzing cash flow projections how much more you really need than you thought.

You decided to forgo venture capital and instead opted to raise funds from private investors, many of whom are women. What advice can you share for entrepreneurs, particularly WOC, on partnering with the right investors, and what do investors need to bring to the table other than just money?

I say this until my face turns blue and people still look at me like I have three heads but choosing investors is like choosing a husband. They are almost identical on legal paper. They own your assets, you share financial responsibilities with them, and ultimately your relationship will be what allows you to succeed or fail. They are not a bank or a cash lender; they are meant to be business partners.

You have to know the type of personalities you vibe with, what their values are, do you have the same humor even. It’s like dating. You have to ask yourself, “Could I be with these people forever? Are they my people? Do they really believe in me and what I am trying to achieve?” These are some of the top questions I ask of my investors when getting to know them and I highly recommend founders do the same when they go out to raise. This is why for WOC especially, it’s important to find your people. The check is secondary to shared values and work style.

You launched Mason Dixie in 2014, and now the brand is available at over 6,000 stores, including Whole Foods, Target, Safeway, Costco, and more. What has been the biggest challenge in scaling your business and what lessons have you learned along the way? What advice can you share on how to scale a business sustainably?

The hardest part about scaling a fast-paced growth business is predicting growth. There are times when you get it dead wrong and over-project, and there are times you go gangbusters and hit it out of the park. Both scenarios are challenging to plan for.

I think the way we have navigated our business growth best was by learning the hard way at first and then optimizing each year. At first, we sprinted and made some mistakes. We were lucky in that the sprint just qualified us for the next race, but we weren’t ready. We just happened to be the fastest runner in that first race. I would have preferred looking back to have trained and prepared for the second race.

So with each misstep, we corrected, learned, and analyzed our weak points and then went in more cautiously. We chose better retailers, improved our product mix, then accelerated. I would always make sure to be cautious. If I could do it again, I would win strategically big and focus on making those wins bigger before going wider. It helps mobilize the team better, focuses your assets, and then allows you to move stronger into new markets.

There are a lot of small business owners reading this interview who would love to have their products sold at major retailers like you. How can these founders follow in your footsteps? What advice can you share for getting a foot in the door with a big-name retailer?

Fair warning: the market has changed a LOT since we first got started. Anyone who started before a couple of years ago were the pioneers. You did a lot and asked for forgiveness later and people were more willing to grow/make mistakes with you.

Now, the world has changed. There is a lot more competition—a lot more products out there—and retailers are getting smarter. Before you go pitch to a big retailer, you have to really know if you are ready. Do you have the marketing and trade budget to support the account? Can you keep up with the volume? Can you afford slotting fees? Do you have a sales support team to monitor and manage the account?

Remember, these players have dealt with far more billion-dollar companies than they have thousand-dollar companies, so the rules are set for much bigger fish than you.

Get educated, get funded, then jump into those waters with caution. Surround yourself with skilled and experienced advisors who have worked in the category/product type you are developing. Ask other companies in those retailers about their experience—both their successes and their follies. Get informed before you pitch.

Where do you think is the most important area for a business owner to focus their financial energy on and why?

Being a founder/CEO means you need to know everything about your business—point-blank. There isn’t one area that is more important than the other. It’s a living system and all parts of the system need to be financially healthy in order for the business to thrive. Now, this doesn’t mean you need to be the expert. Hire a great accountant or CFO early. Allow them to train your eye to see the dark spots and opportunities clearly. Focus on understanding your business over how to be a financial whiz.

What was your first big expense as a business owner and how should small business owners prepare for that now?

People. People people people. They should always be your first biggest expense. Who is helping you to create your projections? Who is going to manage your first order, or even make it? Remember, you cannot do this on your own and the value of the people you surround yourself with will be invaluable in the long run.

What are your top three largest expenses every month?

1. COGs – All of your cost of goods should and will be your largest expense.

2. Trade expenses/marketing – In frozen, we invest a lot into trade since it’s not as easy for us to market and get trial by handing out free sample packs at a metro station or triathlon. Investing back into trade helps us grow and should be one of your largest expenses as you scale.

3. People – Your people should be the best of the best and they deserve to be financially treated as such so they are spending 100% of their time worrying about their business and not if they will get paid. Remember – this industry is tough and financially risky. This is always on the minds of your people so make sure you can pay them on time, and in full.

Photo: Courtesy of Mason Dixie

Do you pay yourself, and if so, how did you know what to pay yourself?

I didn’t pay myself for four years so that others might eat. I lived off of savings and credit cards for as long as I could to ensure I could snag the best people, finance the next purchase order, or invest in the next piece of equipment or manufacturer. I only started to pay myself once I knew I

couldn’t cut checks big enough anymore to fuel the business and took in our first investment, but even then I was conservative and only took what I need to pay rent and eat. As an owner, don’t forget you own the company and that is way more valuable than a salary.

At first, conserve as much cash as you can otherwise you will burn through equity instead. Taking a big salary is a cash burn that will cost you more equity when you need to raise more money before the company has earned the valuation it deserves. So be frugal about what you need in the beginning until the business can afford to pay you.

Would you recommend other small business owners pay themselves?

It just depends on that owner’s personal situation. If I started a business as a single mom with three kids and little savings to live off of, I probably would pay myself the bare minimum I needed to feed my family. But as a single woman with nothing to lose, I lived as bare as I could on what I had. In fact, I worked side hustles until the business could afford to pay for me. It really depends on your financial needs and situation—just be frugal is the biggest advice I can give.

How did you know you were ready to hire and what advice can you share on preparing for this stage of your business?

You are always ready to hire. No one is good at everything. I would have a hard look at your skills and experience, rate those against the different business functions your business needs, and then hire for anything you didn’t rate yourself strongly for. When I took in a business partner, my COO, Ross, I knew I was terrible at operations and needed help. Similarly, when I saw sales ramping up, even though I knew I was good at sales, I only had so much time so rather than spread myself too thin, I invested in the hires knowing that yes, I could still do it, but what was the opportunity cost?

Did you hire an accountant? Who helped you with the financial decisions and setup?

Yes. This should be one of your first hires. I rarely have ever met a founder who is an accountant/financially trained. These people are, you need them. Again, they will educate you about how to look at your business and ultimately help you finance it. They are a critical function.

What apps or software are you using for finances? What’s worked and what hasn’t?

Every business can start with Quickbooks or any off-the-shelf software. In fact, there is a huge market opportunity for you software engineers out there to design scalable accounting software for product companies—hint hint! It’s been fine because of its ease of use and cloud-based

access, but terrible for really using it as a business intelligence and decision support tool. At the end of the day, it’s accounting software, so decision support is still happening in Excel for us. I don’t think there are better solutions until you advance a bit more, but I am always looking.

Do you think women should talk about money and business more? Why?

Yes, we are the biggest consumers in the world! We are business!! More decisions need to be made by the women who LITERALLY hold the purse strings. It can only happen with us talking out loud about it and informing the powers that be how we view money, business, services, etc. The more we show up, the louder we are, the more we will be seen, the more will change.

What money mistakes have you made and learned from along the way?

The funniest mistake was when I thought I was going to be Willy Wonka and open a biscuit factory in just a few months! It was actually one of the best mistakes I ever made. When we sold into Whole Foods our growth was so fast that we were getting requests for products everywhere. Naively, my business partner Ross Perkins and I decided to go after more accounts, particularly in the South because if these biscuits couldn’t sell down there, then we should just call this a good swag item and not further invest. Well, we got both Publix and Kroger to buy our biscuits and were going to go from 100 stores to 1,000 stores in just under nine months. With no idea how to do this, Ross and I leased a drive-thru restaurant with a huge parking lot in the middle of nowhere so we could make pallets of biscuits and store them in a portable trailer freezer on the lot.

We kept doing this for months and transporting the pallets, but the demand kept growing locally, so we couldn’t even keep the inventory we had reserved for the new accounts. I thought we needed to build a bakery! A frozen dough bakery! In the middle of DC! I spent a ton of money on fully engineered plans for this biscuit factory that was also going to have our restaurant attached for the full Ghirardelli experience until we were about to pull the trigger on this huge spiral freezer. Turns out the freezer requires either ammonia or freon—which in DC—are banned in the quantities we needed to fuel this machine. So, we were dead in the water, and we had to pivot to find a way to make biscuits within four months.

I say it was the best mistake I ever made because I ended up being fluent in frozen biscuit production—I knew exactly the equipment I needed, the process, the cost of things—so when I went on the hunt for the facility that would ultimately make our biscuits, I knew everything I needed to know to make the search easy. Because I failed at building a factory, I succeeded in finding the best co-manufacturer out there for our biscuits, and that is what ultimately allowed us to scale and has brought us to where we are today.

What is your best piece of financial advice for new entrepreneurs?

Learn about venture capital and investing before you start. It’s way more complicated, personal, and nuanced than anyone tells you. I did my best to read and research but only as I was hearing no’s during our initial raises. I even did a killer pitch where every investor in the room asked for follow-up discussions. But sometimes it’s not just about your business track record. Sometimes it’s about the color of the money on the table or how much more money is needed and it’s hard to stomach when you think everything else is A+ and you still can’t close the deal.

Anything else to add?

Whenever the going gets tough, ask yourself, what have you ever failed at that you tried your absolute hardest at?

I can’t think of a single time when I put my all into something where I didn’t succeed, so I know if I keep trying, anything can happen. I realized if I didn’t stop trying and if I continued to persevere and stop putting a period at the end of the task, I would ultimately succeed. It’s been the driving statement that through every bad turning point in the path to getting Mason Dixie where it is today, and it is 100% effective.

MORE ON THE BLOG

LLC vs. S Corp: Which Is Best for Small Business Owners?

Picking the right one is essential.

Photo by Marcos Paulo Prado on Unsplash

As a small business owner, you’ve probably heard the words LLC and S Corp floating around. And you probably need to decide which one to form. And while legal structures aren’t the most exhilarating topic, picking the right one is essential for your business.

Deciding if you should go LLC or S Corp starts with knowing the differences between the two and how each one will impact your business. Read on to learn everything you need to know about LLCs and S Corps.

LLC vs. S corp: The basics

As a small business owner, the two legal structures you’ve probably heard the most about are single-member LLCs and S Corps. Before we talk about the difference, we got to get one technical thing straight.

Technically, an S corp isn’t a legal entity but a tax election. It’s confusing but bear with us.

The IRS assigns every business structure a default tax treatment...which is just a fancy way of saying that the IRS decides how each business structure is taxed.

Single-member LLCs are automatically taxed like sole proprietors unless they ask otherwise. That’s where the S corp election comes in.

You can ask the IRS to tax your single-member LLC as an S corp, which means that the IRS won't tax you under the rules of a sole proprietorship; they’ll tax you under the rules of an S Corp (which we'll talk about later).

To keep things simple in this article, we will be referring to:

Single-member LLC as an LLC

Single-member LLC electing to be taxed as an S Corp as an S Corp

Taxes

The biggest difference between an LLC and an S Corp is how you’re taxed.

An LLC and S Corp are both pass-through entities. That means that all the profits from the business are passed on to the owner’s tax return. Unlike a C Corp, which has to pay corporate taxes, your business doesn’t pay any taxes. Instead, you, the owner, do.

How LLC taxes work

The IRS automatically taxes an LLC like a sole proprietorship. Under this tax treatment, you’ll pay two types of taxes:

Self-employment tax - 15.3% of 92.35% of your profit. Self-employment tax goes towards your Social Security and Medicare.

Income tax - Varies based on your tax bracket.

You probably know that self-employment tax is a killer, and it’s why taxes feel so much higher when you’re a small business owner than an employee.

When you’re an employee, your employer pays for half of this 15.3% through payroll taxes, and you pay the other half, which is deducted from your paycheck.

When you’re a small business owner, you pay for all of it yourself.

How S Corp taxes work

When it comes to S Corps, there’s one major tax difference: S Corp owners don’t pay self-employment tax on the business’s profits. They only pay income tax on the profits.

It sounds great, we know. But there’s a catch. S Corp owners are required to pay themselves a reasonable compensation via payroll. And your employee wages are subject to FICA payroll taxes.

FICA payroll tax is 15.3% of your employee wages. Yes, that’s the same amount as self-employment tax. But, the difference is that your business pays half of that (7.65%) through employer payroll taxes, and you pay the other half (7.65%), which is deducted from your paycheck.

You pay the equivalent of self-employment tax, but only on your employee earnings.

There are a few other things to know about S Corp taxation:

Your payroll taxes and the salary you pay yourself are a tax write-off, which lowers your taxable profits.

There’s no federal guideline for reasonable compensation, and we recommend chatting with a tax professional about how much to pay yourself (p.s. Collective can help with this!).

You’ll also have federal and state income tax withheld from your paycheck.

Your income tax will include your employee wages and the profits from your S Corp.

Tax savings: LLC vs. S corp

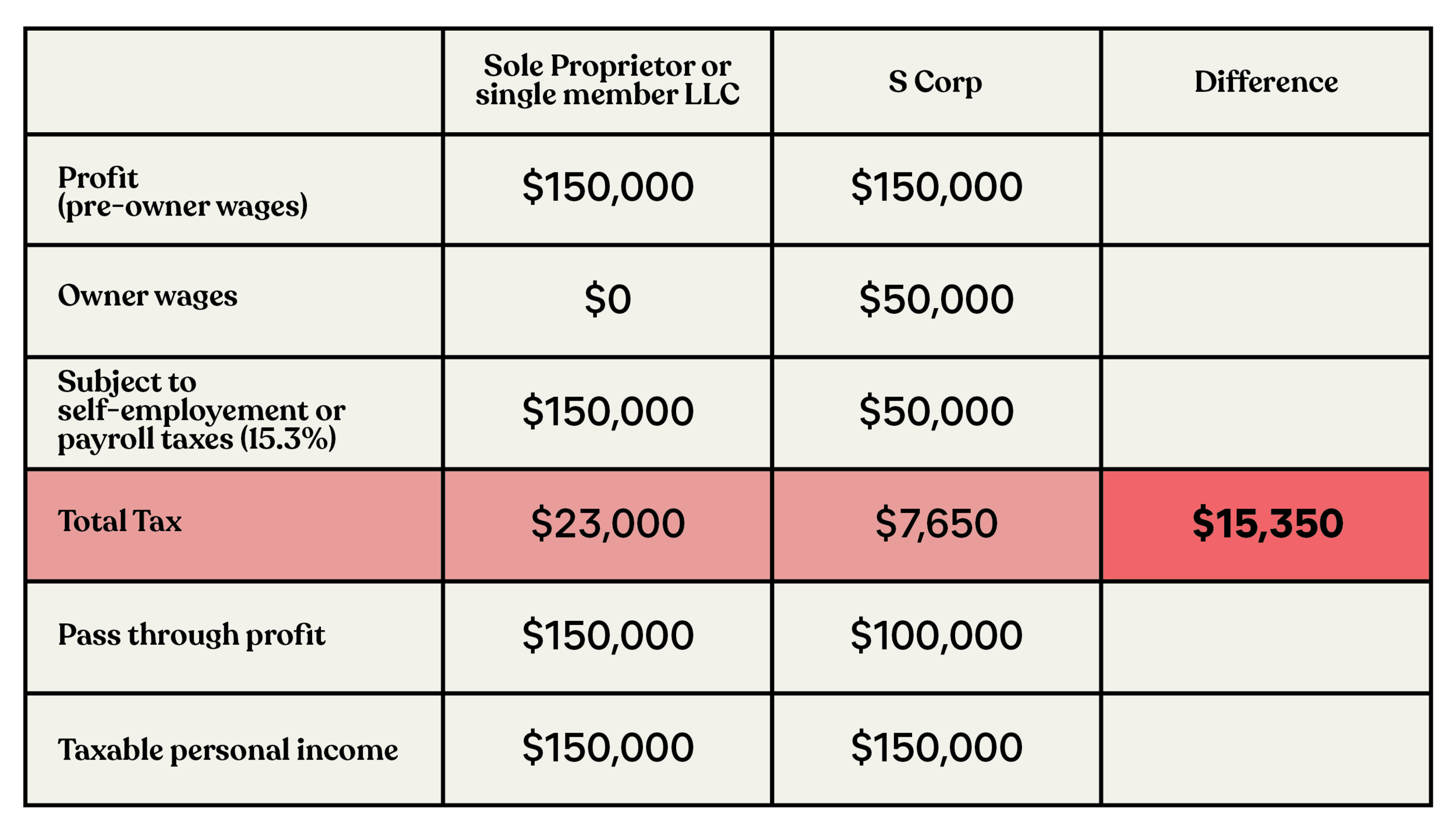

Let’s do an example to compare the taxes a small business owner would pay as an LLC and S Corp. We’re basing this example on a small business owner who earns $150,000 annually in profit and, who as an S Corp, pays themselves a $50,000 salary.

In this example, the business owner could save $15,350 by switching to an S Corp! Keep in mind that these tax numbers don’t include income taxes or state taxes, which will vary based on your tax situation.

If you want a personalized comparison of how much you could save with an S Corp, check out Collective’s tax savings calculator.

Additional costs

S Corps cost more money to run than an LLC. Here are some of the additional costs associated with an S Corp:

Payroll service fees

You 100% don’t want to do manual payroll yourself. Manual payroll involves many percentages, tax calculations, quarterly and annual forms, and ongoing payments to the IRS. If you calculate your payment wrong or miss a deadline, you’ll be subject to a penalty and pay interest on underpayments that you made.

Trust me. It’s way more work than you want to deal with. Instead, you can use a payroll service that runs payroll for you and takes care of all your tax payments and paperwork. Our favorite payroll service is Gusto, which is perfect for S Corp owners.

But like most magical things that do all the work for you, Gusto isn’t free. Gusto will cost you $45 a month to run payroll (unless you have a Collective membership, which includes a free subscription to Gusto).

Bookkeeping costs

The days of doing your bookkeeping via a shoebox full of receipts are over. As an S Corp, you’ll need to get serious about your bookkeeping and use a legit accounting program, like QuickBooks Online. The most basic QuickBooks Online subscription will cost $20 per month (Collective members also receive a free subscription to QuickBooks Online).

Tax preparation fees

When you’re an LLC, you report your business’s income and expenses on your personal tax return, and you only file one tax return.

As an S Corp, you’ll file your personal tax return plus a corporate return called the 1120-S, U.S. Income Tax Return for an S Corporation. Filing this extra return will set you back several hundred dollars.

Annual state registration fees

Depending on where you live, you might have to pay a yearly registration fee for your LLC and S Corp. Fees range from $20- $800 per year.

Cash Flow

S Corps require steady cash flow.

Cash flow is the money that comes in and goes out of your business in a given period. While cash flow includes your income and expenses, it also includes transferring money to your personal account, debt payments, and savings.

Sometimes, businesses are profitable but don’t have enough cash flow to sustain their operations because too much money is going out to cover debt, taxes, or owner pay.

With an S Corp, every time you run payroll, you pay a portion of your taxes in real-time, both as the employer and employee. This means you need to have the money available for your salary and payroll taxes every month.

Liability protection

The good news is when it comes to liability protection S Corps and LLCs offer the same level of limited liability protection to their owners. That’s because an S Corp is an LLC taxed under the rules of an S Corp.

Limited liability means that if your business is sued or can’t pay its debt, creditors and claimants can’t go after your personal assets, like your house or car. While there are some exceptions to this rule, generally, this is the case.

Which one is best for you?

The truth is, the less you earn, the less beneficial an S Corp will be for your taxes. Even if you have some tax savings, the additional costs might eat up all your tax savings. Then you just have more work to do with no payoff.

Our general rule of thumb is that you will benefit from an S Corp if:

You’re earning more than $80,000 in profit each year

You can pay for the additional costs of running an S Corp

You have the cash flow to make regular payroll runs

Now that you have all the deets about LLCs and S Corps, you can make an intentional decision about which entity to form. Still not sure if an S Corp is right for you? Check out Collective’s tax savings calculator and see how much you could save with an S Corp.

C&C readers can enjoy 2 months of a Collective Membership at 50% off with this exclusive sign-up link.

About the Author: Andi Smiles is head of content at Collective. She started her career as a small business financial consultant, teaching businesses-of-one to take control of their finances to build more authentic and sustainable businesses. She’s helped thousands of self-employed folx organize and understand their business finances while also uncovering their emotional relationship with money.

MORE ON THE BLOG

This Founder Never Felt Represented or Celebrated by the Beauty Industry—So She Decided to Do Something About It

And she’s gained the attention of Beyoncé and Sephora in the process.

We know how daunting it can be to start a new business, especially if you’re disrupting an industry or creating an entirely new one. When there is no path to follow, the biggest question is, where do I start? There is so much to do, but before you get ahead of yourself, let’s start at the beginning. To kick-start the process, and ease some of those first-time founder nerves, we’re asking successful entrepreneurs to share their stories in our new series, From Scratch. But this isn’t your typical day in the life profile. We’re getting into the nitty-gritty details—from writing a business plan (or not) to sourcing manufacturers and how much they pay themselves—we’re not holding back.

Photo: Courtesy of Alisia Ford

Alisia Ford was working as an attorney when she launched Glory Skincare, but the business was always more than just a passion project for the first-time founder. As someone who never felt celebrated or represented by the beauty industry, Ford was determined to build a platform for women of color who, like her, had also been overlooked by major beauty brands and retailers. “I wanted to find skincare that worked for women of color and fulfill that huge hole in the beauty industry,” Ford tells Create & Cultivate. “It was almost a moment of, ‘If not me, then who?’ and that’s when I knew I had a responsibility to create this space in beauty for ‘her.’”

But Glory Skincare is more than just a platform to shop clean skincare. “We carefully curate products with dermatologists and chemists with specialties in skin of color and even work with psychologists so we can positively build up the relationship between skin and mental health,” Ford explains. “I prioritize making sure that women are creating self-care rituals based on what they really want, not what marketing agencies want them to buy.” And her conscientious approach has gained the attention of two of the most influential names in beauty, Beyoncé and Sephora. As a brand that’s been featured in Beyoncé’s Black Parade Route and graduated from Sephora's accelerate incubator program, Glory Skincare is a beauty brand to watch in 2021 and beyond.

Ahead, Ford tells Create and Cultivate how she bootstrapped the business, what she learned from the Sephora accelerate program (mentorship is everything), and why it’s important to invest in the future success of your business.

Can you tell us a bit about your background and what you were doing professionally before launching Glory Skincare?

Before Glory Skincare, I had a long career as an attorney. Most recently, I was an attorney for Apple’s advertising agency, but I’ve also served in various roles at premier organizations, such as Nike, Fox Sports, and Disney, across a broad range of industries. I’m so glad that I took the leap to leave my attorney days behind me and launch Glory Skincare. Being a woman in business has been so rewarding because I’m always surrounded by other incredible and supportive women.

How did you come up with the name Glory Skincare? What are some of the things you considered during the naming process?

The naming process for Glory was pretty easy but there is always a lot to consider when naming a company. I needed something that would be easy to recognize, but also reflected the vision and values of the brand. I wanted this company to be a community where women of every color and background are celebrated because, for many years, I never felt represented or celebrated by the beauty industry. It has taken me many years to find a sense of peace and belonging. This journey to self-acceptance has been a gift from God and the name glory is a personal reminder of this opportunity. Glory means great beauty and splendor which is how I want my community to feel in this new kind of beauty movement.

What were the immediate things you had to take care of to set up the business?

After I had the initial plan for Glory, I wanted to jump right in but I knew it wouldn't serve the business well to rush into things. I started out by writing a detailed business plan that helped me to understand the values, mission, and goals for Glory. Part of writing this business plan was also spent doing a lot of market research. Glory is intended to be a reflection of what my community wants. I dedicated a lot of time connecting with women of color about their skin to listen and understand the top concerns and problems they all face. Luckily, my background in the legal industry prepared me well for all of the paperwork you have to do for trademarking, finances, etc. Other immediate things I did were setting up the Glory Skincare domain and social media channels, hiring a team, and working on the marketing and design elements of Glory.

What research did you do for the brand beforehand? Why would you recommend it?

Because Glory Skincare is meant to create a space for women of color that changes our relationship with beauty for the better, I made a decision from the very beginning to be very mindful about every aspect of our actions that could affect the women in this community. Even though my own experience as a Black woman helped me make the initial realization that a community like Glory was necessary, our adherence to this standard meant that we had to do additional market research, learn from dermatologists, and work rigorously with psychologists.

How do you find and identify the brands that you stock? What do you consider during this process and why are these factors important to you and your business?

Glory Skincare is a community for women of color, and all of the brands and products on our site reflect that. We carefully curate products with dermatologists and chemists with specialties in skin of color and even work with psychologists so we can positively build up the relationship between skin and mental health. I prioritize making sure that women are creating self-care rituals based on what they really want, not what marketing agencies want them to buy.

How did you identify the manufacturer you work with to create Glory’s line of products? Are there any mistakes you learned from along the way and what advice can you share for aspiring entrepreneurs on finding the right partner to create a product?

When looking for a manufacturer, take your time and don't settle for something you don't want. Bringing on a team of people you trust and work well with is essential if you want the business to succeed. As a people person, it was really important to me that I had a good relationship with the manufacturers. The key things I looked for in the manufacturing company we hired were attention to detail, flexibility, problem-solving, and dependability. I am really lucky to work with a great manufacturer and I think this is because I really took the time to do the research and find the right company that aligned with my vision and goals for Glory.

How did you fund your business? What were the challenges and what would you change? Would you recommend that route to other entrepreneurs?

At the beginning, I was bootstrapping the business but I knew we would need to begin fundraising in order to grow the business to where I wanted it to be. It was challenging to be launching a business with such little funding available but it pushes you to be resourceful and work as efficiently as possible. We managed to raise a pre-seed round of capital but recently, my time and energy have been devoted to our seed funding. Fundraising is challenging and feels like a full-time job itself but it's been rewarding to have investors really connect with the brand and believe in the mission of Glory.

Photo: Courtesy of Glory Skincare

How big is your team now, and what has the hiring process been like? Did you have any hiring experience before this venture? If not, how did you learn and what have you learned about it along the way?

We’re a small but mighty team! Right now, we have about five people on the team full-time but have a board of dermatologists, a team of manufacturers, and a PR team that we work with as well. Hiring during a pandemic can be difficult. It's hard to really connect with someone when you are interviewing over Zoom. I did not have much experience with hiring before this so there has been a lot to learn along the way. During an interview, it's important to ask questions pertaining to the job but I think we often forget it's important to also ask questions to help get to know the candidate on a more personal level. Someone might look great on their resume, but if you are bringing them onto your team, you also want to make sure they are someone you can trust and get along with.

Did you hire an accountant? Who helped you with the financial decisions and setup?

I do have a financial team that helps with investments, deposits, financial planning, etc. Since I do not have a background in finance, I knew I needed to hire an accountant to help with the financial side of the business. Just like with any member of your team, it’s important that you trust this person with the success of your business. Find someone who aligns with your values and believes in your company as much as you do.

What has been the biggest learning curve during the process of establishing your business?

This may sound a little cliché, but the amount of time and energy that goes into a business is something you can’t really anticipate. Every day is a new challenge and my toughest but most important lesson was definitely flexibility.

How did you promote your company? How did you get people to know who you are and create buzz?

Shortly after we launched, we were featured on Beyonce's website in the Black Parade roster of Black-owned businesses. That was such a highlight of this whole journey and really ramped up the business. Last summer, I hired a PR team to help with securing press coverage for Glory. From product placements to founder interviews, their team has really helped get the name of Glory out into the media landscape.

You recently graduated from Sephora's accelerate incubator program—congratulations! What was the experience like for you and how has it impacted your business? Tell us everything!

It’s been such a great experience and an amazing opportunity that I’m so thankful for. The program has been extremely helpful. We’ve received advice on everything from financial statements, to branding, to operations and fulfillment. As a cohort, we've created a bond as all founders of color and every individual in the program is someone I respect and value. I am beyond grateful for the experience! The program was intense and we all dedicated many hours to attending seminars, workshops, and meetings with various industry experts and professionals. I was pushed outside of my comfort zone but in the best way possible. The future of Glory is brighter than ever before thanks to the program.

Do you have a business coach or mentor, and would you recommend one?

I have a handful of really incredible mentors and advisors that I have met along the way. I am a part of several entrepreneurial groups and programs that have put me in touch with other founders that I have been able to lean on for support and guidance. I recently graduated from the Sephora Accelerator program which introduced me to people who are experts in their respective fields. As a brand founder, it's easy to forget that we are not experts in every aspect of the business. Having mentors, coaches, and leaders to go to for advice and support will help you make more educated decisions that will benefit your business greatly. I am grateful that I have a space to learn about what it is like to start a business, share ideas with other dreamers, and get encouragement to take a leap of faith.

What is one thing you didn’t do during the setup process that ended up being crucial to the business and would advise others to do asap?

Don't try to do it all alone. When I first launched Glory Skincare, I was fired up about my idea and tried to manage and oversee every element of the business. This wasn't sustainable and I quickly realized that I was burning myself out. Having a team is everything. Everyone can bring their unique talents, skills, and experiences to the table and build each other up in a really inspiring way.

What is your number one piece of financial advice for any new business owner and why?

Invest in the long-term success of your business. At first, it’s hard to see so much money going into development, branding, marketing, operations, etc., but these investments will pay themselves off in the long run. If you set yourself up for success, it will come with time and effort.

MORE ON THE BLOG

These Founders Are Bringing Fair Labor Practices, Artisanal Jobs, and Economic Development to Tunisia

Alia Mahmoud and Lamia Hatira are investing in their “tiny but mighty Mediterranean country.”

You asked for more content around business finances, so we’re delivering. Welcome to Money Matters where we give you an inside look at the pocketbooks of CEOs and entrepreneurs. In this series, you’ll learn what successful women in business spend on office spaces and employee salaries, how they knew it was time to hire someone to manage their finances, and their best advice for talking about money.

Photo: Courtesy of Fouta Harissa

When Alia Mahmoud and Lamia Hatira met, they felt an immediate kinship. “We each have a Tunisian father and an American mother and our lives were sort of mirror images,” says Mahmoud. “Lamia was born and raised in Tunis and spent time in Seattle growing up, while I grew up in New York City and spent summers in Mahdia, Tunisia,” she elaborates. Although both women live abroad today—Mahmoud in Miami and Hatira in São Paulo—their families still live in Tunisia, and the textile brand Mahmoud and Hatira founded, Fouta Harissa, is their way of investing in their “tiny but mighty Mediterranean country,” Mahmoud tells Create & Cultivate. But they’re not just investing capital, they’re investing in fair labor practices for the country’s artisanal community.

By working with Tunisian artisans to craft high-quality, hand-loomed textiles, the brand is dedicated to preserving artisanal weaving in Tunisia while also contributing to the country’s economic development. “Unfortunately, Tunisian artisans are generally undervalued and underpaid as the custodians of our cultural heritage,” explains Mahmoud. “We want to change that by bringing the world a modern take on handmade artisanal products that also support fair labor practices, use sustainably sourced materials, and contribute to economic development in Tunisia,” she notes. Not only that but each of the artisans they work with is employed in a full-time position at the brand’s partner workshop and paid an above-market rate that exceeds the living wage.

Ahead, Create & Cultivate asks the co-founders all about how they self-funded the socially-driven brand, why they recommend hiring an accountant ASAP, and what money mistake has taught them the biggest lesson.

How did you fund Fouta Harissa? What were the challenges and what would you change? Would you recommend your route to other entrepreneurs?

Lamia Hatira: We started with a small friends-and-family investment of $20,000 which helped us start our entities in both Brazil and the U.S.A. We are definitely still working on a small budget. It’s challenging because you don’t have the resources to do everything you want to do right off the bat, but it’s also kind of wonderful because you learn what really matters for your business and how to make the most of what you have.

Each experience is definitely unique, but if you have an opportunity to get seed investment from friends and family at the initial stages, embrace it. Just make sure you’re on the same page with your investors about how active a role they will play and get in writing in your operating agreement.

The most important thing is to do what you’re comfortable with. We knew we weren’t ready to take out a huge loan or ask for a larger amount at the beginning because we didn’t want to owe anyone money or give away too much equity before we knew more about the intricacies of our business.

Three years later, we are now ready to take on more investment because of everything we’ve learned and because we know what works and doesn't work for Fouta Harissa at this stage.